Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of Contemporary Management

On-line version ISSN 1815-7440

JCMAN vol.13 n.1 Meyerton 2016

RESEARCH ARTICLES

Factors affecting the sustainability of independent financial planners in KwaZulu-Natal Province, South Africa

KM PeterI; M HoqueII, *

IGraduate School of Business and Leadership University of KwaZulu-Natal KPeter@oldmutual.com

IIGraduate School of Business and Leadership University of KwaZulu-Natal hoque@ukzn.ac.za

ABSTRACT

A large number of independent financial planners are leaving the industry permanently or joining alternative models. The aim of this article was to determine the factors affecting independent financial planners on the sustainability of independent financial planners.

This was a cross-sectional study conducted among 525 independent financial planners practising in the long-term insurance industry in KwaZulu-Natal province, South Africa. A self-administered, anonymous questionnaire was distributed via QuestionPro software program. A total of 115 participants completed the questionnaire.

Results had shown that legislation was a key factor affecting independent financial planners. A quarter of respondents indicated that they had considered exiting the industry within the last five years and among them 73% reported compliance legislation as the major reason. One third of respondents experienced a decrease in income over the last five years with 60% confirming that commission regulations negatively impacted on their income. Over half of the respondents agreed that clients are using alternative channels for the purchase of insurance products.

Independent financial planners need to incorporate social media and other forms of technology in their practices for the marketing, distribution and sale of products and services to retain and attract new clients.

Key phrases: alternative channel; financial planner; insurance industry; insurance products; legislation compliance

1. INTRODUCTION

The financial services sector impacts all citizens of South Africa (SA). It stimulates economic growth and job creation. It fosters the building of infrastructure and sustainable development for SA. This sector facilitates daily economic transactions enabling people to save and preserve wealth for goals (Department of National Treasury 2011:1-85).

According to the Department of National Treasury (2011:1-85), the financial services sector comprises banks, insurance companies, investment companies, pension funds, securities markets and regulators.

In South Africa the financial service sector comprises over R6 trillion in assets and contributes 10.5% of the gross domestic product of the economy annually. It employs 3.9% of the employed South Africans and contributes at least 15% of corporate income tax (Department of National Treasury 2011:1-85).

2. LITERATURE REVIEW

Independent financial planners have been subject to various challenges in recent years. Costs to distribute insurance products through independent financial planners are viewed as high. Legislation implemented to regulate the industry is perceived as complex and voluminous (Financial Services Sector Assessment Report 2014:1-108). Consumer expectations and buying preferences are changing.

The emergence of non- traditional or alternative channels like direct insurers, online sales, telemarketing and bank financial planners are challenging the market share of independent financial planners (Financial Services Sector Assessment Report 2014:1-108).

In South Africa, financial service sector comprises over R6 trillion in assets and contributes 10.5% of the gross domestic product of the economy annually. It was estimated that total employment in the banking sub-sector amounted to approximately 157 000 in 2011 which was up from around 155 000 in 2010, with Investment Banking contributing to 11% of the total number for 2011, while Retail Banking accounted for the remaining 89% (Financial Services Sector Assessment Report 2014:1-108).

2.1 International perspective

Financial planners provide advice to people in respect of wealth creation and retirement planning (Hawkins 2003:1-32). Jonathan Dixon, Deputy Director of the Financial Services Board (FSB), states that "A key element of adequate consumer protection is the value of good advice and the FSB places a high value on independent advice to consumers" (Van Flymen 2013:22). Independent financial planners help the public understand the investment and risk options available to meet their financial goals.

The absence of independent financial planners could affect the goals of wealth creation (Hawkins 2003:1-32). Further, Melzer (2006:Internet) states that the lack of professional financial advice provided to consumers could result in inadequate provision for death, disability, retirement and general savings. This could place a strain on the financial resources of the government because people who have not saved sufficiently would become dependent on the government social age pension. A sound financial plan prepared in consultation with an accredited professional financial planner would prevent the public from becoming dependent on government social grants. The demise of independent financial planners could result inadequate financial planning services being available to the public and at an unaffordable cost.

Internationally there has been a decline in the market share of independent financial planners around the world except the middle and east European countries. In the United Kingdom (UK), sales of insurance products by independent financial planners decreased from 90% to 73% over the first decade of the 21st century. Less than 60% of insurance products were sold through independent financial planners in 2005 in the UK (Gentle 2007:84-86).

2.2 South African perspective

The financial planning industry in SA is in the process of evolving from a sales orientated industry to a fully-fledged financial planning profession. In the past, a person selling insurance products only required product knowledge and sales skills. Today, the same individual has to be a financial planner providing financial planning advice to clients on estate, retirement, investment and business planning. Independent financial planners have to move from salesman to planners, educating clients and assisting them with financial planning decisions and purchases.

2.3 Factors influencing the decline of independent financial planners

The reasons identified for the decline of independent financial planners are: legislation (compliance, education and commission), technology (mobile, internet and telemarketing), competition from direct insurers, tied or franchise planners and bank employed advisors, and customer perceptions and expectations of independent financial planners.

These reasons are substantiated by the Broker Confidence Index 2013 undertaken by CIB Insurance Administrators. This measures the confidence level of insurance brokers on a number of issues concerning the South African economy and the insurance industry. According to this survey, 31.9% of brokers view regulations as the biggest challenge for insurance brokers in South Africa. A further 28.3% cited direct insurers and 30.1% cited the economy (CIB 2012:Internet).

2.3.1 Legislation

Legislation has negative and positive effects on financial planners. There is a need for consumer protection and as such relevant legislation is required. It does ensure economic stability, consumer protection, transparent access to financial services and the assurance that entities and individuals operating and practising in the industry are correctly licensed and registered.

Regulations are implemented to rectify market failures, ensure economic stability and provide consumer protection (Schiro 2006:25-30). As such, the South African government introduced legislation to regulate the financial services industry. The objective of legislation is to provide a safer financial environment, to ensure public protection and foster confidence. A well-regulated financial system is vital for financial stability and sustainable economic growth.

The South African financial services industry has become subject to various pieces of legislation. Legislation ensures that the public has access to financial services providers who are correctly licensed and registered. It also ensures that fees and commission payable are fair and transparent. The object of consumer protection requires professionalism in respect of the participants in the financial services industry. Benfield (1999:Internet) stated that legislation similar to FAIS introduced in the UK and Australia resulted in almost 40% of financial planners exiting the industry.

2.3.2Financial planners' commission debate

Commission compensation is related to the signing of a contract and conditional on the payment of a premium (Focht, Richter & Schiller 2013:329-50). According to Schwepker and Good (2010:299-317), monetary reward is viewed as a motivator that impacts on a salesperson's actions and decisions.

Financial planners may engage in mismatching uninformed consumers with inappropriate insurance companies. This will be done if it is profitable and increases payoffs (Focht et al. 2013:329-50). This could lead to a conflict of interest and ethical problems. The financial planner may be biased towards a particular insurer or product where he or she is not remunerated for the advice provided to consumers but receives a commission from the insurer. This could create wealth for the planner but the product may be inappropriate for the customers (Tseng & Kang 2014:26-42).

High commissions are paid to financial planners on the assumption that an insurer will have the business on books for approximately 10 years. However, in some cases 50% of such policies lapse after 4 years and these policies will not result in profits (Gentle 2007:84-86).

2.3.3Technology use in financial planning

Channels such as call centres, internet and mobile devices are becoming attractive for marketing, distribution and sale of insurance products to the public. The internet, mobile devices and social networks have gained prominence over the past decade. This has contributed to the birth of a new generation of consumers who want simplicity, speed and convenience for their financial interactions. As such, consumers use online channels for the purchase of products (Ernst & Young 2012:1-20).

The financial services industry has adopted new channels through the developments in technology (Hughes 2006:113-129). In the UK, non-traditional channels have negatively affected the traditional independent financial planner channel. The market share of independent financial planners decreased from 90% to 73% and in 2004 over 60 billion pounds of premiums related to the life and pension industry were generated through alternative channels. Further less than 60% of life insurance was sold through independent financial planners compared to 93% in 2000 (Gentle 2007:84-86).

2.4 Motivation for the study

The South African insurance broker industry is facing a potential crisis because a significant number of independent financial planners are leaving the industry permanently or joining alternative models. According to the Financial Services Board (FSB), there are approximately 12 000 licensed financial planners in SA with less than 20% younger than 35 years old (Coetzer 2013:Internet).The average age of the South African financial planner is 54 years old and equates to more than 70% of the planners.

Thus in the next five to ten years many of the financial planners in SA would have retired (Institute of Practice Management 2012:1-29). There is a decrease in the number of new entrants into the industry (Coetzer 2013:Internet). This will put pressure on independent financial planners' succession and continuity plans. According to Field, Froser and Kolarl (2007:3646-62), the broker market is declining due to the changing regulatory environment. Therefore, the objective of this study was to determine the factors affecting independent financial planners to leave the industry in KwaZulu-Natal, SA.

3. RESEARCH METHODOLOGY

Since no previous study conducted among independent financial planners in KwaZulu-Natal-this study focussed on the independent financial planners working in KwaZulu-Natal, SA. Independent financial planners provide financial planning advice to consumers. This includes advice on estate, retirement, investment and business planning as well as on disability and dread disease protection. The advice entails the sale of products to satisfy any shortcomings or gaps identified.

Planners have to be licensed by the FSB to market, distribute and sell insurance products. The approval of the license depends on the planner possessing the appropriate qualifications and experience. Planners should have contracts with at least two or more insurance companies to justify their independence (otherwise they would be seen as tied agents of a particular insurance company). Further, independent financial planners require accreditation from the various product providers' to be able to sell these product providers' products.

3.1 Population, samples and data collection

The population for this research study was the independent financial planners practising in the long term insurance industry in KwaZulu-Natal province. The reason for this is that Old Mutual is one of the largest financial service providers in South Africa and one of the researcher was working for the company.

The population was 525 independent financial planners who have contracts to market, distribute and sell Old Mutual risk and investment products. No sampling method was used as the population size was part of the study. The self-administered, anonymous questionnaire was sent to all the independent financial planners via QuestionPro program which is an online survey instrument. A letter of consent accompanied to the questionnaire. Two reminders were forwarded to respondents who did not complete the questionnaire after the initial e-mail invite.

3.2 Data collection instrument

The questionnaire was divided into five sections. The first section pertained to demographic details. Second section consisted of legislation, followed by technology, alternative channels and the final section consisted of clients' expectations and perceptions of independent financial planners (independent financial planners' perspective) on how financial planners perceive the career of financial planning.

3.3 Pre-testing of the questionnaire

The questionnaire was pretested amongst the regional manager of Broker Distribution, in KwaZulu-Natal province, two legal advisors and three independent financial advisors to reveal the weaknesses of the measuring instrument. Therefore, it was the researcher's assumption that five people would be good to pre-test the questionnaire. This was done to ascertain the duration of time that would be spent on completing the questionnaire. Further, improvements were made to the questionnaire on recommendations from the pilot study group.

3.4 Ethical issues

Ethical clearance was obtained from the University of KwaZulu-Natal. A gatekeeper's letter was obtained from the Regional Manager of Broker Distribution, KwaZulu-Natal to use the Old Mutual's database of independent financial planners. The questionnaire was accompanied by a letter of consent. Participants were advised of confidentiality and anonymity. Further, participants were allowed to exit the questionnaire at any stage. Participation in the study was voluntary.

3.5 Data analysis

Initially data were exported to SPSS program for analysis. Descriptive statistics such as frequency distribution was run for all the variables. Chi-squared test of association was carried out to find association between two categorical variables. A p-value <0.05 was considered statistically significant.

4. RESULTS AND DISCUSSION

A total of 525 questionnaire was sent via online survey instrument to all the independent financial planners. Only 115 completed questionnaires were received. Therefore, the response rate was 22%.

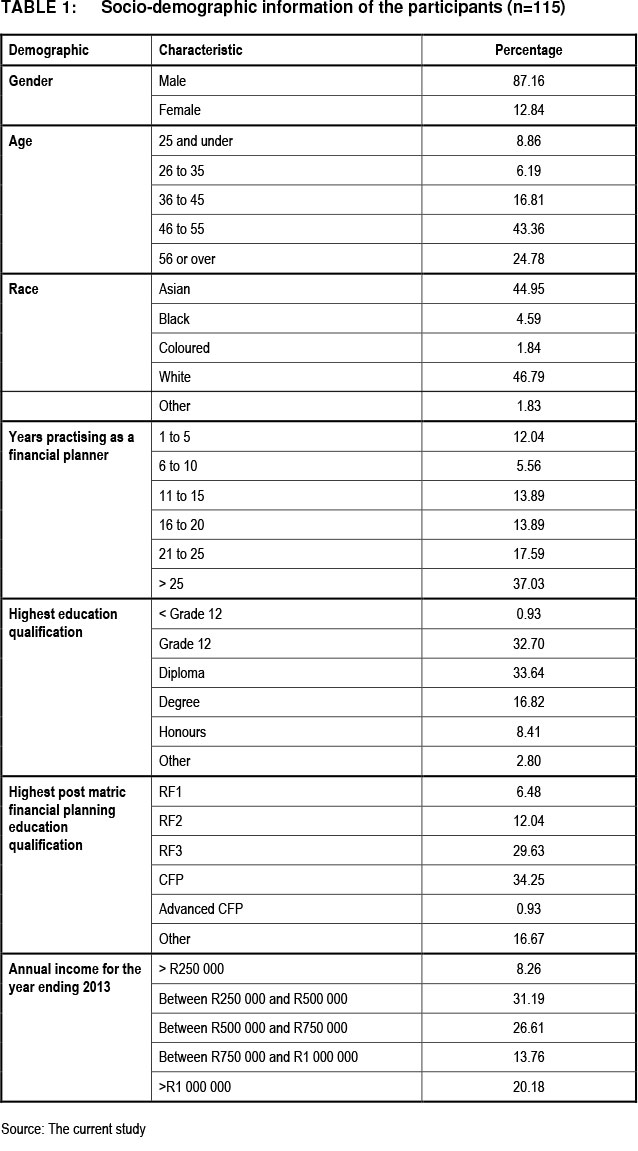

Table 1 shows the summary of socio-demographic informations of the respondents. Results indicated that the independent financial planning industry in KZN is a male dominated industry, with over 88% of the respondents being male. Majority (77%) of the respondents are over 45 years with the average age of respondents being approximately 51 years. This supports the finding of survey conducted by the Institute of Practice Management (2012:1 -29) that found that the average age of planners was 54 years. This supports the view of Bird (2014:Internet) that independent financial planning as a career was on the decline. This is a cause for concern as it indicates that the industry is an aging one with fewer people entering the industry or becoming independent financial planners.

It was found that 67% of all respondents either possess a grade 12 secondary qualification or a one year diploma. The results indicate that a third of the respondents had a diploma as their highest educational qualification. This contrasts with the Institute of Practice Management survey (2012:1-29) that found that 92% of respondents did not further their post matric qualification. This could be due to this study being restricted to independent financial planners in KZN, whilst the former survey included all types of financial planners practising in the financial services sector throughout the country.

Over half of all respondents earned between R250 000 and R750 000 in 2013, with approximately 31% earning between R250 000 and R500 000. At least one fifth earned over R1 000 000. In terms of the survey undertaken by the Institute of Practice Management (2012:1-29), independent financial planners' profit margins are decreasing due to legislative requirements.

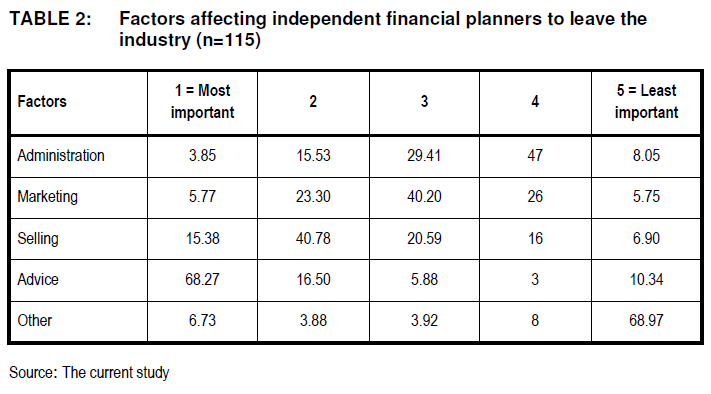

Table 2 indicates that over two thirds of respondents view the advice component of their job as the most important. Selling and marketing rank as the second and third most important functions in an indepedent planner's praticise. The is in line with the requirements of FAIS legislation that requires planners to provide advice to clients before the sale or marketing of a product (Part VII of the General code of conduct for authorised financial service providers and representatives - FAIS Act).

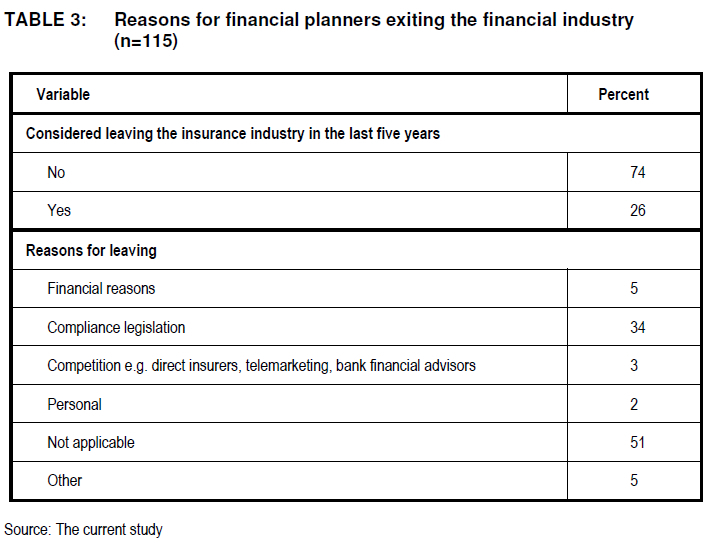

Over one quarter of all respondents have indicated that they had considered exiting the industry within the last five years (Table 3). Of those planners that considered exiting the industry, compliance legislation is cited as the most popular reason (73%) for exiting the industry (table 3).

These findings are in line with Institute of Practice Management (2012:1-29) that found that regulatory compliance costs are adversely affecting independent financial planners. In addition the findings of this study confirm the findings of the Coredata survey (2014:Internet) where it was found that independent financial planners were exiting the industry because of compliance legislation.

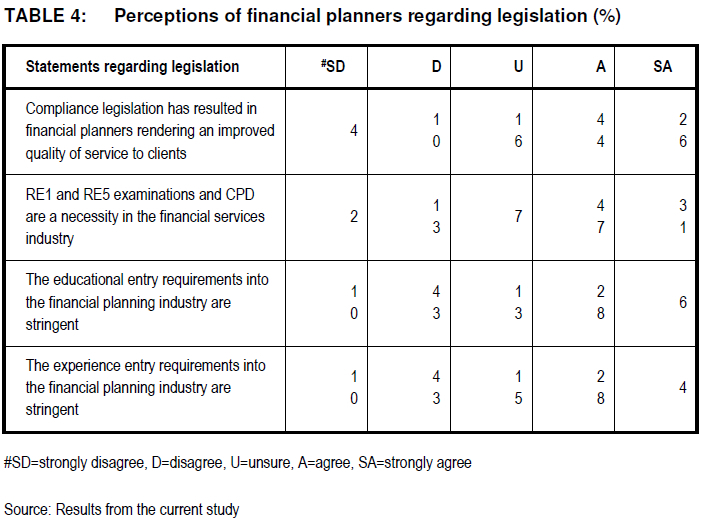

Table 4 shows that 70% of respondents either agree or strongly agree that compliance legislation has resulted independent financial planners rendering an improved quality of service to clients.

This is in line with the purpose of the TCF. TCF was implemented to ensure that all stakeholders in the insurance industry design and sell appropriate insurance products to the public. This supports the literature review that found that compliance legislation does promote consumer protection ensuring economic stability, as stated in the Department of National Treasury policy document (2011:1-85), "A Safer Financial Sector to Serve South Africa Better".

It was found that almost one third of all respondents either agree or strongly agree that the educational and experience entry requirements are stringent (table 3). This is in line with the results of the Coredata survey (2014:Internet) that found that planners have a wealth amount of industry experience but do not have the required financial planning qualifications.

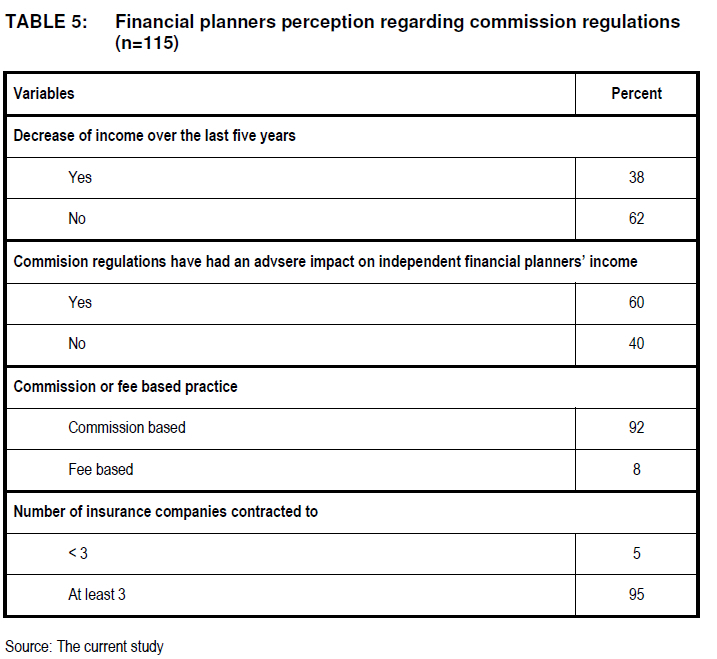

Further, the Coredata survey's results confirmed that due to educational requirements 15.7% will resign from their current roles, 3.9% will exit the industry and 7.8% are undecided about their future. Finanial planners have to comply with the fit and proper requirements (experience and educational qualifications) in terms of the FAIS Act to practise as a financial planner. However, it is evident that this compliance aspect of the FAIS Act is viewed as stringent by independent planners. Over one third of all respondents experienced a decrease income over the last five years (Table 5).

Sixty percent of all respondents positively reported that commission regulations have negatively impacted on their income . This is line with the commission regulations where commission payable on investments policies effected after 1st January 2009 is limited to 2.5% payable upfront and 2.5% paid as and when premiums are received (LTA).

Further, these findings support the research conducted by Coredata (2014:Internet) that revealed that 57.9% of independent financial planners view commission regulation as their biggest challenge.

Less than 10% of respondents have adopted a fee based practise, which may become a rule with the future Retail Distribution Review legislation. This supports the findings of the Coredata survey of 2013 where it was found that only 12.8% work on fee based model.

Almost all (95%) of the respondents were contracted to market, distribute and sell at least three or more insurance companies' products (Table 5). This may be in line with good business practice requiring financial planners to provide clients with at least three quotes from different product providers.

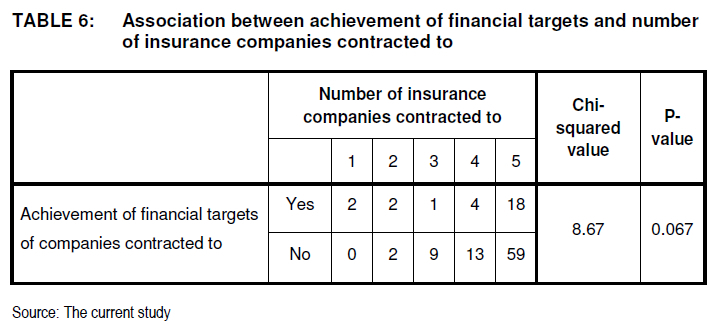

Table 6 indicates that about 70% of all respondents have more than 4 contracts. Industry practice requires independent financial planners to present clients with a minimum of three quotes from three different companies.

However, this table indicates that the more contracts an independent financial planner has, the less likely he or she was to meet the financial targets of those insurance companies with whom he or she had contracts.

To remain contracted with insurance companies and to have a face to face business consultant service an independent financial planner, the planners have to write business of a set minimum amount (which differs from company to company) This may be onerous. Thus independent financial planners are found wanting due good business practice determined by industry expectations.

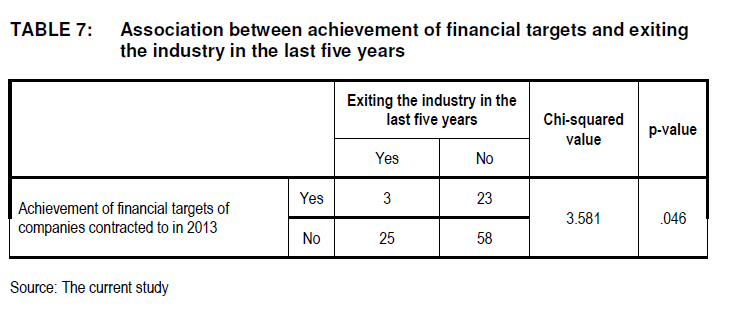

Table 7 indicates that almost 90% of respondents who did consider leaving the insurance industry in the last five years did not meet the financial targets of the all the insurance companies with whom they had contracts in 2013. Further, 71% of repsondents who did not intend leaving the industry in the last five years did not meet the financial targets of all insurance companies with whom they had contracts in 2013. Insurance companies include a financial target in the contract granted to an independent financial planner. If planners fail to meet this target certain services and benefits associated with having a contract with that insurance company are not provided. Industry practice dictate that independent financial planners provide clients with three quotes from three different companies. However, if they are unable to meet the financial targets of the companies, they face the risk of having their contract suspended, wirhdrawn or cancelled. This could lead to them exiting the industry due to them not having a minimum of three insurance contracts.

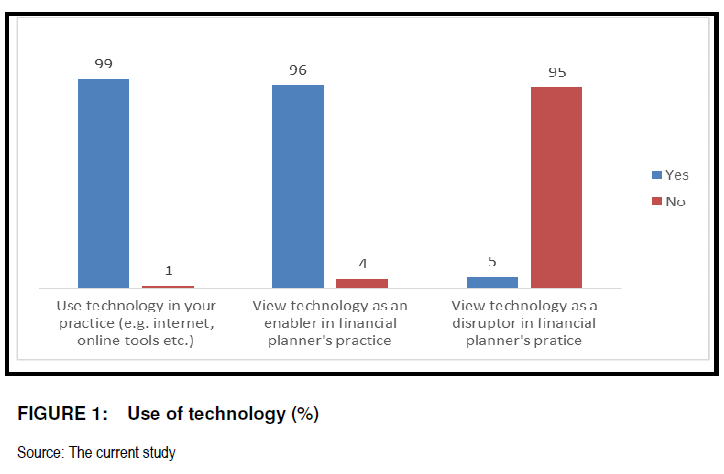

According to figure 1, almost all repondents use some form of technology in their practise (99%), and 96% perceived technology as an enabler in their practices. This supports the view of Deloitte (2013:1-8) that states technology facilitates a client centric approach affecting every stage of the buying process.

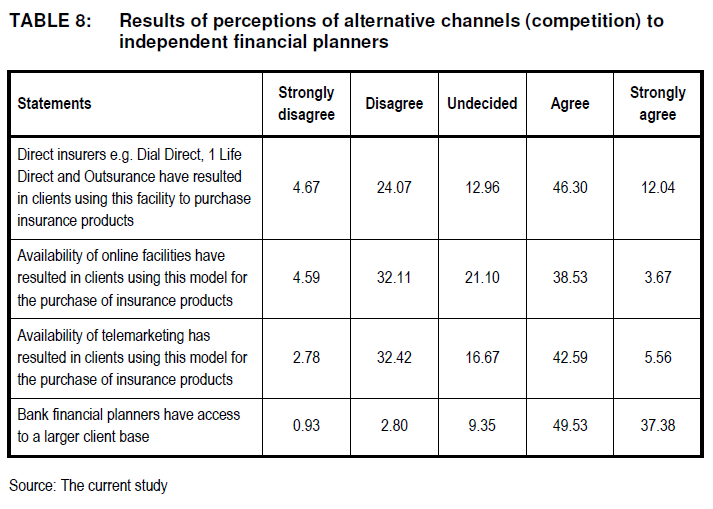

Views in respect of alternative channels (competition) on independent financial planners are summarized in table 8. It was found that 56% of all respondents agree or strongly agree that clients are using direct insurers to purchase insurance products, and 42% of respondents either agreed or strongly agreed that consumers were using online facilties to purchase insurance products. This supports the results of the Capgemini survey that found that customers now use the internet for research and purchase of insurance products (Capgemini 2013:1-48).

Further, according to a survey conducted by Deloitte in 2010, direct channels allow insurance companies to increase sales whilst keeping costs low. The findings also support the views of Stone, Kiran, Brew & Selby (2002:387-401), and Easingwood and Storey (1996:211-24) who hold that insurance companies are using various distribution channels to keep costs low and to reach a wider market.

Almost half (48%) either agree or strongly agree that clients make use of telemarketing to purchase insurance products. This supports the survey of Deloitte (2010:1-20) that telemarketing is emerging as a prominent alternative distribution channel. Over 86% of respondents agree or strongly agree strongly agree that bank financial planners have access to a larger client base.

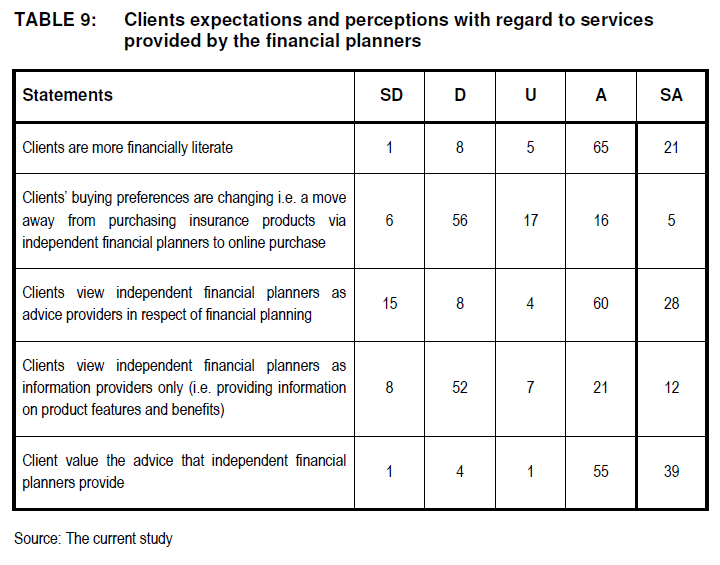

Approximately 86% of respondents either agree or strongly agree that clients are more financially literate (Table 9). However, in terms of Figure 4.24, 62% of all respondents either strongly disagree or disagree that clients' buying preferences are changing (i.e. a move away from indepedent financial planners to online purchases). This contrasts with the Capgemini study that found consumers prefer to use low cost more convenient channels to purchase financial products (Capgemini 2013:1-48).

5. RECOMMENDATIONS

The following recommendation are made based on the study findings:

■ Tertiary institutions in the province could incorporate subjects or courses related to financial planning in the curriculum of applicable degrees or diplomas. The tertiary institutions in KZN could offer the Diploma and the Advanced Diploma in Financial Planning as is offered by the Universities of the Free State, Stellenbosch and Nelson Mandela bay or the Nelson Mandela University.

■ There has to be a concerted effort on the part of all stakeholders to professionalise the industry. The legislation that has been enacted is a step in the right direction. The minimum qualifications required to practise as a financial planner will result in confidence and trust on the part of consumers in the profession and the independent financial planners practising in the profession.

■ Legislation regarding the fee based model (RDR) needs to be embraced by independent financial planners as means to professionalise the industry. This will give credibility and add value to the profession.

■ Consumers need to be made aware of legislation highlighting the financial planning process. Emphasis should be placed on educating consumers on the use of independent financial planners to better meet their financial goals. Consumers must be educated as to the impartiality on independent financial planners who are in licensed to sell products of more than one insurance company.

■ Independent financial planners need to incorporate social media and other forms of technology in their practices for the marketing and sale of products and services to retain and attract new clients.

■ Finally, further research should be conducted amongst consumers or purchasers of insurance products to determine their perceptions and expectations of the financial planning industry.

6. STUDY LIMITATIONS

There is a lack of academic literature on factors affecting the independent financial planners, particular in South Africa. This could be due to the fact that financial planning is a relatively new profession.

The population was limited to independent financial planners in Kwazulu-Natal that have contracts with Old Mutual. This may not include all independent financial planners in the province as not all independent financial planners have Old Mutual contracts. It did not include those operating in the short term insurance industry. These planners would face similar challenges as they are subject to the same factors affecting those that practice in the long term insurance industry. Therefore, the results of the study should be interpreted with caution.

7. CONCLUSION

The findings of the study indicate that the there are various factors that impact on the independent financial planners. Legislation, technology and alternative channels are identified as key factors for sustainability of the financial planners. Clients' financial literacy affects independent financial planners by placing additional demands on their practices. Respondents are divided on clients' expectations for their commission or fees to be discounted.

REFERENCES

BIRD G. 2014. South African regulation - has it gone too far? [Internet: http://www.sablog.kpmg.co.za/2013/10/the-south-african-regulatory-landscape-has-it/; downloaded on 2014-01-13. [ Links ]]

BENFIELD B. 1999. Insurance legislation and the demise of the industry. The Development Group of Southern Africa, South Africa. [Internet: http://www.freemarketfoundation.com; downloaded on 2014-01-14. [ Links ]]

CAPGEMINI. 2013. World insurance report. Capgemini:1-48. [ Links ]

CIB. 2012. Brokers confident about business conditions. Business Live. [Internet: http://www.cib.co.za/News-Blog/Blog/Brokers_confident_about_business_conditions; downloaded on 2014-01-13. [ Links ]]

COETZER J. 2013. Right steps needed now to ensure future of independent broker. [Internet: http://www.sanlam/co/za/wps/wcm/connect/sanlam_en/sanlam/media+centre; downloaded on 2014-01-08. [ Links ]]

COREDATA. 2014. SA Adviser Efficiency 2013. [Internet: http://www.coredataresearch.co.za/view/sa-adviser-efficiency-2013/; downloaded on 2014-02-25. [ Links ]]

DELOITTE. 2006. Face to face with the future. Deloitte:1-20. [ Links ]

DELOITTE. 2010. More than one approach - alternative insurance distribution models in Asia Pacific. Deloitte:1-20. [ Links ]

DELOITTE. 2013. Recognising RDR reality - the need to challenge planning assumptions. Deloitte:1-8. [ Links ]

DEPARTMENT OF NATIONAL TREASURY OF THE REPUBLIC OF SOUTH AFRICA. 2011. A safer financial sector to serve South Africa better. Department of National Treasury:1-85. [ Links ]

ERNST & YOUNG. 2012. Voice of the customer - time for insurers to rethink their relationships. Ernst and Young Global Consumer Survey 2012. Ernst and Young:1-20. [ Links ]

EASINGWOOD C & STOREY C. 1996. Distribution strategies in the financial services sector. Journal of Financial Services Marketing 1 (3):211-224. [ Links ]

FIELD LP, FROSER DR & KOLARL JW. 2007. Bidder returns in bank assurance mergers: is there evidence of synergy? Journal of Banking and Finance 31 (12):3646-3662. [ Links ]

FINANCIAL SERVICES SECTOR ASSESSMENT REPORT. 2014. Growth, regulation, compliance, skills and recruitment in South Africa. [Internet: https://www.westerncape.gov.za/assets/departments/economic-development-tourism/fssa_report_18march.pdf; downloaded on 2016-06-30. [ Links ]]

FINANCIAL PLANNING STANDARDS BOARD (FPSB). 2009. Global perspectives - the state of the financial planning profession in the "post-trust" era. Financial Planning Standards Board:1-23. [ Links ]

FOCHT U, RICHTER A & SCHILLER J. 2013. Intermediation and (mis)matching in insurance marketing - who should pay the insurance broker. The Journal of Risk and Insurance 80(2):329-350. [ Links ]

GENTLE C. 2007. The distribution dilemma - why insurance companies need to change their business models. The Journal of Risk Finance 8(1):84-86. [ Links ]

HAWKINS P. 2003. South Africa's financial sector ten years on: the performance of the financial sector since democracy. Trade and Industrial Policy Strategies, Feasibility:1-32. [ Links ]

HUGHES T. 2006. New channels/old channels: Customer management and multi-channels. European Journal of Marketing 40(1/2):113-129. [ Links ]

INSTITUTE OF PRACTICE MANAGEMENT. 2012. The cost of financial advisory business compliance in South Africa. Institute of Practice Management:1-29. [ Links ]

MAAS P. 2010. How insurance brokers create value - a functional approach. Risk Management and Insurance Review 13(1):1-20. [ Links ]

MELZER I. 2006. Consumer trust in the life industry: is the glass half empty of half full? [Internet: http://www.eighty20.co.za/insightout/consumer-trust-in-the-life-insurance-industry; downloaded on 2014-03-15. [ Links ]]

SCHIRO JJ. 2006. External forces impacting the insurance industry: threats from regulation. Geneva papers on risk and insurance - The International Association for the Study of Insurance Economics. Issues and Practices 31(1):25-30. [ Links ]

SCHWEPKER CH jr & GOOD DJ. 2010. Transformational leadership and its impact on sales force moral judgement. Journal of Personal Selling and Sales Management 30(4):299-317. [ Links ]

STONE M, KIRAN C, BREW T & SELBY D. 2002. Managing customers in retail bank branches. In Foss B and Stone M (eds). CRM in Financial Services. Kogan Page: London. Pp. 387-401. [ Links ]

TSENG LM & KANG YM. 2014. The influences of sales compensation, management stringency and ethical evaluations on product recommendations made by insurance brokers. Journal of Financial Regulation and Compliance 22(1):26-42. [ Links ]

TSU-WEI Y. 2014. Partnerships between life assurers and their intermediaries. Management Research Review 37(4):385-408. [ Links ]

VAN FLYMEN B. 2013. Sound financial advice is crucial to protect consumers. FIA Insight 2nd Quarter:22. [ Links ]

* corresponding author

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}