Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Business Management

On-line version ISSN 2078-5976Print version ISSN 2078-5585

SAJBM vol.55 n.1 Cape Town 2024

https://doi.org/10.4102/sajbm.v55i1.4565

ORIGINAL RESEARCH

The composition of listed family firm boards in South Africa: Alignment to best practices and governance codes

Gabriela dos SantosI; Suzette ViviersI; Elmarie VenterII, III

IDepartment of Business Management, Faculty of Economic and Management Sciences, Stellenbosch University, Stellenbosch, South Africa

IIDepartment of Business Management, Faculty of Business and Economic Sciences, Nelson Mandela University, Port Elizabeth, South Africa

IIIFamily Business Unit, Faculty of Business and Economic Sciences, Nelson Mandela University, Port Elizabeth, South Africa

ABSTRACT

PURPOSE: As elsewhere in the world, family firms (FFs) play a critical role in the South African economy. There is, however, scant research on how, if at all, listed South African FFs differ from their non-family counterparts concerning board composition and independence. The purpose of this study was to address this knowledge gap by investigating director and chair independence, chair-chief executive officer (CEO) role duality, board race and gender diversity, as well as board rotation at FFs listed on the Johannesburg Stock Exchange (JSE) over the period 2006 to 2022. The study was informed by the agency, socioemotional wealth, and stewardship theories

DESIGN/METHODOLOGY/APPROACH: Data were collected on 753 directors who served on the boards of 37 JSE-listed FFs. Data sources included Bloomberg and the FFs' integrated reports and websites. Data were analysed by examining trends in the considered variables over time

FINDINGS/RESULTS: While family involvement at board level remained relatively constant, considerably fewer family members served as board chairs and CEOs towards the end of the research period. Board independence increased significantly over the research period

PRACTICAL IMPLICATIONS: Shareholder activists' requests for improved board governance of JSE-listed FFs seem justified. Activists should, however, also consider the benefits of family stewardship when evaluating director and chair independence in these firms. This study also identifies practical implications for nomination committees and investor education

ORIGINALITY/VALUE: The use of multiple theoretical lenses provides a balanced view of board governance at JSE-listed FFs. The study contributes to the scant body of knowledge on board composition and independence in listed FFs in South Africa, which will enable future FF research

Keywords: board independence; board tenure; corporate governance; family firm governance; principal-principal agency conflicts; socioemotional wealth preservation; stewardship; transparency.

Introduction

Although it has been estimated that the majority of family firms (FFs) in developed and developing economies are small- and medium-sized businesses (Venter & Hayidakis, 2021), a substantial number of publicly listed firms around the world are under the direct control of families (Benjamin et al., 2016). Empirical studies indicate that the concentration of ownership within a family is common among listed firms and predominant among FFs. The FFs also have a strong presence in South Africa where it is estimated that 60% of publicly listed firms on the Johannesburg Stock Exchange (JSE) are FFs (Rabenowitz et al., 2018). Given their substantial contribution to economies worldwide, scholars have shown a growing interest in FF-related research in the last two decades (Molly & Michiels, 2021; Sherlock et al., 2022; Rovelli et al., 2021). While a plethora of definitions exist to define an FF, most include some measure of family ownership (the percentage of shares held) or family involvement in management and decision-making structures and processes, including the board (Acquaah & Eshun, 2016; Andersson et al., 2018; Arteaga & Escribá-Esteve, 2021).

Compared to non-family firms (NFFs), FFs have two distinct characteristics. Firstly, FFs have the intention to pass the business down to successive generations. Secondly, there is a constant interaction between the family, business and ownership systems (Metsola et al., 2020). Daspit et al. (2021) thus are of the opinion that FFs have unique succession intentions, non-financial goals, governance structures and outcomes compared to NFFs. In recent years, the number of studies investigating FF heterogeneity has also grown substantially, showing that FFs differ from one another in, among others, their non-economic goals, socioemotional wealth (SEW), values, governance configurations and family-generational-interpersonal exchange (Daspit et al. 2021).

In the global context, many scholars have compared listed FFs with non-FFs in terms of board diversity and independence (e.g., Garcia-Meca & Santana-Martin, 2023; Khadija, 2022; Robino et al., 2017). However, in South Africa it is almost impossible to do a comparative study, as no complete list of JSE-listed FFs (Mashele, 2021) and previous research on board composition of these firms exists. As such, it is practically impossible to compare listed FFs with NFFs to identify the impact of the family on financial performance or to assess differences in respect of corporate governance outcomes such as an ethical culture, effective control and legitimacy (Institute of Directors South Africa [IoDSA], 2016). Researchers and regulators, nonetheless, underscore the importance of studies on board independence and diversity as these provide potential means of improving corporate governance (Khadija, 2022). Shareholder activists are however, increasingly criticising JSE-listed firms for failing to improve on these board characteristics (Cassim, 2022; Davids & Kitcat, 2023; Viviers et al., 2019).

Several well-known JSE-listed FFs have been targeted by shareholder activists in recent years. Many of these firms created pyramid structures in the 1950s and 1960s to preserve the founding family's control and thwart hostile takeover bids (Hasenfuss, 2008). Activists have argued that these control structures are costly and show no respect for modern corporate governance standards (Hasenfuss, 2008). While most of these control structures were dismantled in the mid-2000s, some are still firmly in place.

Investors who are concerned about board ineffectiveness can use a range of activist strategies to bring about change. Gornsztein and Likhtman (2020) emphasise that:

Investors care deeply about how well a company board is functioning. Getting this aspect of governance right makes it more likely that material risks and opportunities will be well managed. It follows that an effective board is best placed to secure a company's long-term success. (p. 2)

As the most influential investors, shareholders can initiate change by voting against the election of certain directors, asking questions at shareholder meetings, and requesting private negotiations with key decision makers (Martini, 2021). As in many other common law countries, shareholder activism in South Africa primarily takes place behind closed doors (Cassim, 2022; Mans-Kemp & Van Zyl, 2021; Shingade et al., 2022; Yamahaki & Frynas, 2016). More instances of public activism are, however, found in these countries especially among activists striving to improve corporate governance policies and practices.

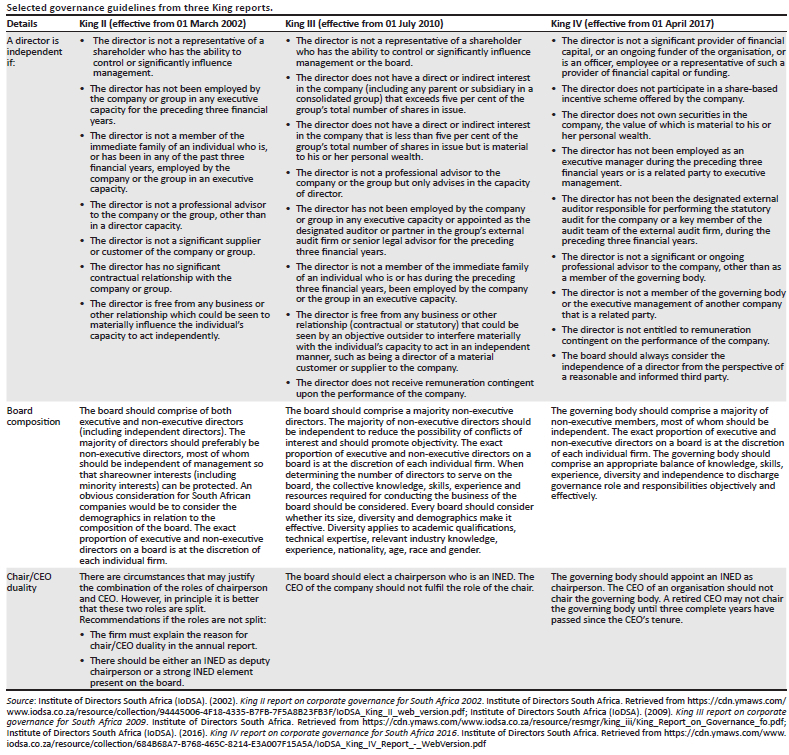

All JSE-listed firms, irrespective of their ownership and control structures, should comply with the governance guidelines contained in the King reports. King I was the first report published in South Africa in 1994 and contained non-legislative codes that were to be applied through a principle-based approach (Ntim, 2013). This report was updated in 2002 to accommodate rapid changes in information, communication and technology. Despite the voluntary nature of King I and II, both reports resulted in changes to the JSE's listings requirements. Since the first report, JSE-listed firms have been urged to appoint independent non-executive directors (INEDs) to monitor and address opportunistic managerial behaviour (IoDSA, 1994). Independent non-executive directors are also called outside or unaffiliated directors. Firms have also been encouraged to split the roles of board chair and chief executive officer (CEO) to improve managerial oversight and avoid potential conflicts of interest (Davids & Kitcat, 2023; IoDSA, 2016, 2009).

In FFs, however, board chairs and CEOs are often family members (Kerai et al., 2023). In addition to assuring that the business under their management stays competitive, these individuals also experience pressure to preserve the family chain, power, culture and heritage (Corbetta & Salvato, 2004; Curado & Mota, 2021; Farrington et al., 2020). Some family board chairs and CEOs have been very successful in achieving these divergent goals (Farrington et al., 2020). The presence of family members on the board and in executive positions have furthermore been shown to enhance financial performance and improve loyalty and goodwill among customers, employees, suppliers and local communities (Aronoff & Ward, 2016; Berrone et al., 2012; Kang & Kim, 2016; Sageder et al., 2018).

Given the benefits of family involvement in the highest decision-making echelons of FFs, is it justified to hold them to the same corporate governance standards as their non-family counterparts? Consider the example of Simon Susman who dedicated 37 years of his life to Woolworths Holdings. In 1934, Simon's grandfather, Elie Susman and brother Harry, bought their first shares in the South African clothing retailer, ushering in an eight-decade-long association with the firm. During Simon's decade at the helm (2000-2010), the firm's share price rose from R2.60 to over R26.00 (Buthelezi, 2018). After Susman's retirement as CEO, shareholders elected him as non-executive board chair. After stepping down from this position in 2019, he continued to provide support and advice to the board free of charge and continued to devote his time to advancing Woolworths' participation in civil and corporate society (Crotty, 2019). Local shareholder activist Theo Botha criticised Susman's appointment in 2010 on the grounds that the chairperson should be an INED (Marais, 2010). Susman's affiliation with the founding family and long tenure as CEO of the business clearly disqualified him as being an INED (IoDSA, 2009).

Given the importance of listed FFs in the South African economy, scant research on how, if at all, JSE-listed FFs differ from their non-family counterparts concerning board composition, governance, heterogeneity among FFs, calls by shareholder activists for enhanced board independence and transparency exist. This descriptive study, thus makes several theoretical and practical contributions. Firstly, this study contributes to the limited literature on listed FFs in South Africa and aims to present a more balanced view on the complex topic of FF governance as suggested by Arteaga and Escribá-Esteve (2021). Secondly, this is the first study of its nature in South Africa, making use of not only of traditional theories such as the agency theory but also the socioemotional wealth (SEW) and stewardship theories to investigate the influence of the family on board practices. Thirdly, the empirical evidence will enable future researchers to determine the influence of these board practices on firm's performance and other outcomes of listed firms, and compare listed FFs in South Africa with their non-family counterparts. The latter is necessary to add to the global debate whether FFs and the family themselves, have a positive or negative influence on board practices and the financial and social performance of the business. Several practical recommendations are made on how South African JSE-listed FFs could improve their board composition and independence.

Secondary data were hand collected from the integrated reports and corporate websites of 37 JSE-listed FFs over the period of 2002-2022. This time frame was chosen as it covers governance guidelines contained in three King reports (II, III and IV). Focus was placed on director independence, chair independence, chair-CEO role duality, board race and gender diversity, and board rotation. Annexure A provides extracts from the relevant King reports on these governance guidelines. The following section is dedicated to defining FFs, highlighting their importance and presenting arguments for and against stricter board governance at these firms. Arguments are rooted in the agency, SEW, and stewardship theories. The methods used to collect and analyse data are then outlined. Key findings are presented thereafter along with suggestions for nomination committees and non-family directors serving on the boards of JSE-listed FFs, governance activists, policymakers and scholars.

Family firms and board composition

Listed FFs often face criticism regarding the family's control over strategic and operational decisions (Carney et al., 2015). In South Africa, listed FFs have also been slated for the slow pace of governance reforms in this regard (Crotty, 2019, 2021; Marais, 2010). Whereas the requirement for JSE-listed firms to have a unitary board structure has remained unchanged since 2002 when King II became effective (IoDSA, 2002), several amendments were made to the categorisation of individuals appointed as INEDs in subsequent reports. King III and King IV explicitly state that the board should comprise a majority of non-executive directors, most of whom should be independent (IoDSA, 2016, 2009). Under the King III regime, nomination committees had to use a set of disqualifying (or factual) criteria to gauge a director's independence. Under King IV, independence became a matter of perception (Green & Moodley, 2021). Post-2016, JSE-listed firms thus had more leeway in categorising non-executive directors as independent.

King IV states that an INED may only serve in an independent capacity for longer than 9 years if the board concludes that the director 'exercises objective judgement' and that:

[T]here is no interest, position, association or relationship which, when judged from the perspective of a reasonable and informed third party, is likely to influence [the INED] unduly or cause bias in decision-making. (IoDSA, 2016, p. 13)

This assessment must be conducted on an annual basis and included in the integrated report. As of 2010 (when King III came into effect), firms have been urged to split the roles of board chair and CEO. The chair should also be an INED (IoDSA, 2009). The board should furthermore establish arrangements for periodic, staggered rotation of members to invigorate its capabilities with the expertise and perspectives of new directors, while retaining valuable knowledge, skills and experience.

The need for unaffiliated directors and chairs to monitor managerial behaviour and regular board refreshment are deeply rooted in the agency theory (Dah et al., 2023; Fama & Jensen, 1983; Kilincarslan, 2021; Molly & Michiels, 2021). Governance codes based on the agency theory call for the creation of board structures and practices that will ensure that the board is a distinct entity, capable of objectivity and able to act separately from management. These governance codes place a high value on board independence and transparent reporting (Kerai et al., 2023).

The applicability of agency-based governance mechanism in the FF context has, however, been challenged as family members often occupy board and top management positions. Lane et al. (2006), for example, demonstrated that some agency-based governance reforms introduced in the United States in the early 2000s were detrimental to family unity. Researchers such as Chrisman et al. (2018) and Dinh and Calabrò (2019) hence call for a closer inspection of the unique formal and informal governance structures present in FFs when reviewing governance quality.

Scholars should notice that family members in top management positions often support their kinsman despite sub-par job performance (Bendickson et al., 2016). Altruistic motives may also explain why FFs appoint relatives to managerial positions rather than more qualified, non-family candidates. These appointments are based on relational contracts that include mutual expectations based on emotional and sentimental considerations (Morgan & Gomez-Mejia, 2014). Many instances have been cited of family managers pursuing non-financial interests such as protecting the family's reputation, cohesion and power at the expense of minority shareholders. In some cases, family entrenchment has given rise to family managers not being held accountable to the same governance standards as their non-family counterparts (Gomez-Mejia et al., 2011; Morgan & Gomez-Mejia, 2014). These types of principal-principal conflict adversely affect the interests of non-family shareholders (Bendickson et al., 2016; Bhattacharyya et al., 2014; Neckebrouck & Schulze, 2018).

The SEW theory is a behavioural agency theory and suggests that the family is motivated by, and committed to, preserving their SEW and that the family derives affect-related value from its controlling position in the firm (Berrone et al., 2012; Gómez-Mejía et al., 2007). Boardroom decisions relating to control and influence, stakeholder relationships, business venturing and corporate governance have been shown to be affected by the intended preservation of SEW (Hasenzagl et al., 2018). Two SEW dimensions in particular, family influence and control, and dynastic succession, explain why FFs appoint family members to the board and in executive positions (Naldi et al., 2013).

Although the appointment of family members as board chairs or CEOs may aid FFs in preserving their socioemotional endowments, it reduces board independence Berrone et al., 2012; (Kilincarslan, 2021; Naldi et al., 2013). The first dimension (family influence and control) also sheds light on why FFs tend to appoint fewer INEDs than NFFs (Jong & Ho, 2019; Kilincarslan, 2021; Shaw et al., 2021). King IV acknowledges that 'emotive issues' and entrenchment could drive decision making in FF boardrooms and propose the appointment of INEDs to mitigate this risk (IoDSA, 2016, p. 107).

In contrast to the agency and SEW theories, the stewardship theory proposes that managers are good stewards who do not require additional monitoring (Madison et al., 2016). This theory promotes a more relaxed approach to board governance. Less emphasis is placed on board independence and carefully crafted executive remuneration packages as managers are seen as individuals who take their responsibilities seriously. Jasir et al. (2023, p. 278) go as far as saying that managers should not be viewed as 'greedy' but rather as individuals who act altruistically for the collective good of the firm. The stewardship theory does not regard chair-CEO role duality as problematic and supports the appointment of specialist executive directors (Clarke, 2004).

Some scholars have shown that low levels of board independence at listed FFs may even reduce agency costs between family and non-family principals; the argument being that family-elected directors closely monitor managers on behalf of all shareholders irrespective of their ties with the family (Jong & Ho, 2019). Habib et al. (2019) further suggest that some FFs appoint INEDs simply to signal good governance. In light of the mixed empirical evidence regarding board governance at FFs (Dinh & Calabrò, 2019; Jasir et al., 2023; Lane et al., 2006; Madison et al., 2016) and the lack of studies in South Africa, further research on the topic was warranted.

Research design and methodology

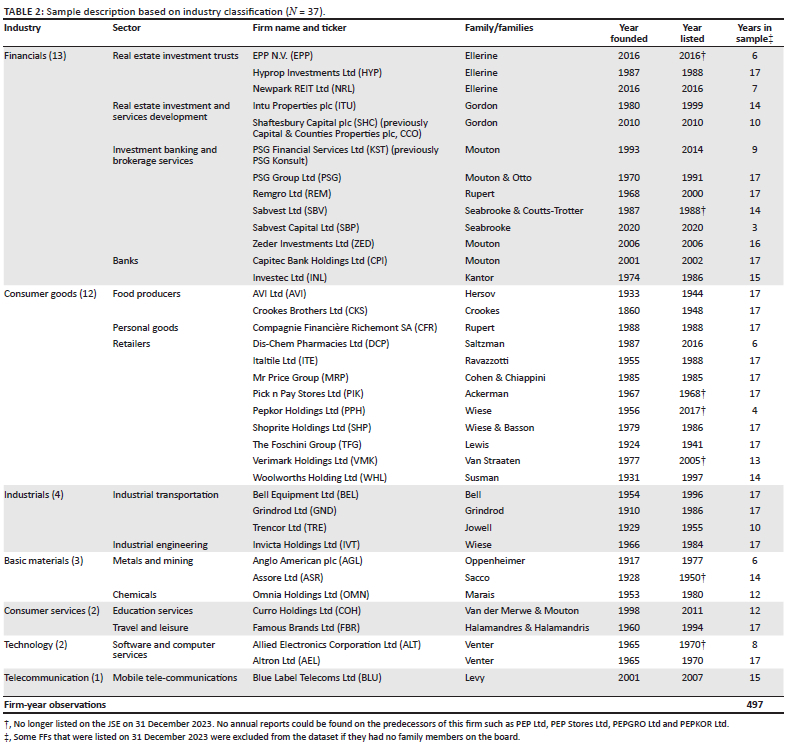

No sample frame reflecting the population of JSE-listed FFs exists (Mashele, 2021). The authors were, however, able to extend an existing database in which an FF was defined as a JSE-listed firm with at least one family member on the board (Viviers, 2022). Keywords such as 'family firm', 'family business empire', 'business tycoon', 'family-owned', 'family-controlled', 'heir(s)', 'successor(s)', 'founding family', and 'Bros' were used to identify additional FFs from articles published in credible online financial newspapers, magazines and industry reports. The sample was thus constructed based on data availability. Family firms that were suspended or that delisted during the research period (2006-2022) were included in the dataset to address potential survivorship bias. Data on industry association and year of establishment were collected from the FFs' integrated reports and websites and other credible sources.

The following data were hand collected for each of the 753 directors who served on each of the 37 identified FFs' boards for each year that the firm was listed: name, status (executive; non-executive; INED); date appointed to the board, gender (man; woman), race (person of mixed race; white), whether the director was the CEO (1;0), whether the director was the board chair (1;0), and whether the director was a member of the founding family (1;0).

The surnames of women directors who got married or divorced during the research period were carefully checked to avoid double counting. A director's gender was determined by examining photos and references to 'Mr', 'Ms', 'Mrs', 'he/him' or 'she/her' in the FFs' integrated reports. In instances where no identifying data were disclosed, websites and other online resources, such as LinkedIn and Who's Who of Southern Africa were consulted. The authors acknowledge the shortcomings of this approach in that directors could have gender identities and roles other than those described as 'man' or 'woman'. A director's race was determined by referring to Section 9(5) of the Broad-Based Black Economic Empowerment Act (No. 53 of 2003).

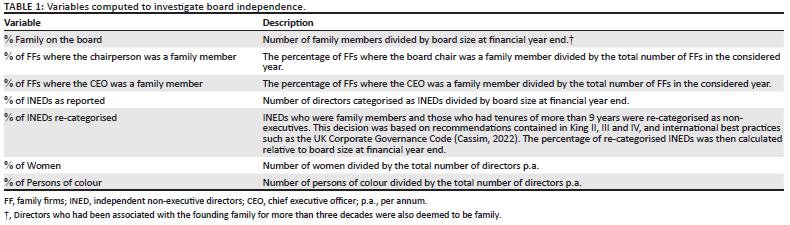

Each director's tenure was determined by comparing the year under consideration with the year in which he and/or she was appointed to the board. Table 1 provides a description of other variables computed. Two proxies were considered for director independence, namely percentage of INEDs as reported and percentage of INEDs re-categorised.

The nature of family involvement was also determined. A board was classified as intergenerational where family members from different generations served concurrently. An intragenerational board had family members from the same generation, such as siblings or cousins, serving side by side. Data were furthermore sourced from the Bloomberg database on board rotation, that is the maximum number of years that a director may serve before he and/or she is required to stand for re-election. The unbalanced panel dataset was analysed using descriptive statistics, mixed model analysis of variance (ANOVA) tests.

Sample description

As shown in Table 2, most of the sampled FFs operated in the financials and consumer goods industries (35.14% and 32.43%, respectively). While the Ellerine and Venter families have concentrated their efforts in single industries, others (such as the Mouton, Wiese and Rupert families) own businesses in unrelated industries.

Grindrod and Crookes Brothers were the two oldest FFs in the sample. Both firms were established more than a century ago. The median age of the considered FFs in 2022 was 51 years. This observation reflects tenacity and agility on the part of FFs to weather numerous political and economic storms in the country's history.

Whereas some FFs make no reference to the founding family, others are very proud of their origins and continued association with the family. In their 2022 integrated report (p. 14), the board chair of Famous Brands for example, mentions that the firm began as a family business in the 1960s and adds that it has 'in many ways retained the essence of comradery'. Famous Brands, which had the largest number of family directors of all the sampled FFs, includes franchisees and employees in its definition of 'family'. Several tributes to individuals who passed away in the preceding year state that they will be sorely missed by the 'Famous Brands family'. Many of these individuals were affiliated with the FF for decades lending support to the notion that FFs often enjoy high levels of loyalty from non-family employees (Aronoff & Ward, 2016; Neckebrouck & Schulze, 2018).

Results

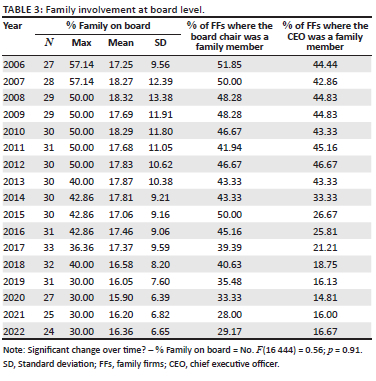

In the majority of FFs, a successor was the only family member on the board. Several examples of intergenerational and intragenerational boards were observed. In most intergenerational boards, fathers and son(s) served concurrently. Most family members were second generation and often served alongside a parent, sibling or child. As illustrated in Table 3, the average percentage of family board members remained relatively constant at 16%. Table 3 also reflects the outcome of the mixed model ANOVA, which was used to determine whether there was a statistically significant change in this variable over the research period.

Considerably fewer family members were board chairs and CEOs towards the end of the study period. In 2022, less than a third (29.17%) of the sampled FFs' chairs were family members and a mere 16.67% had a family member as CEO. Kang and Kim (2016) found a similar trend among family-controlled Chaebols in Korea from 2001 to 2011. These scholars noted that Chaebols were more likely to replace family CEOs with non-family CEOs when they experienced deteriorating financial performance. With fewer family members in the 'driving seat', impartiality in board decision-making might have improved.

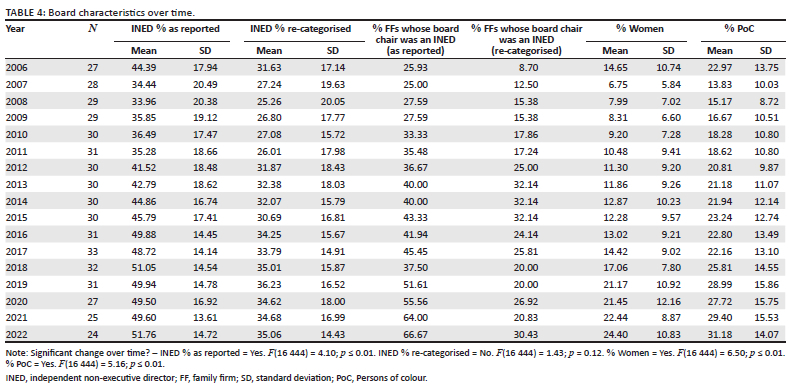

The findings in Table 3 contradict some studies (e.g., Berrone et al., 2012; Morgan & Gomez-Mejia, 2014; Shaw et al., 2021), which suggest that FFs prefer to maintain control of these two key positions to ensure the renewal of family bonds to the firm through dynastic succession. Details on important board characteristics over time are presented in Table 4. Except for one, all FFs separated the roles of board chair and CEO. From a corporate governance perspective, this result is welcome as policies such as King IV suggest the separation of the two roles (IoDSA, 2016). The splitting of these two roles allows for increased skills, experience and critical evaluation of boardroom decisions (Mandato & Devine, 2020). Approximately one fifth of the sampled FFs required directors to stand for re-election on an annual basis. This board rotation requirement is important from the agency perspective as it encourages regular board refreshment and enhanced impartiality (Dah et al., 2023). Board refreshment can improve board capabilities as new directors with fresh perspectives and expertise are appointed while maintaining important skills and institutional knowledge (IoDSA, 2016). From the principal-principal conflict point of view, board refreshment may also enhance the confidence of minority shareholders in the board as they can see that their interests are also being considered. Details on important board characteristics over time are presented in Table 4.

In line with previous South African FF scholars (Viviers, 2022), a significant increase is observed in the proportion of INEDs in terms of the FFs' own director categorisations (F [16 444] = 4.10, p ≤ 0.0). Although the percentage of INEDs based on kinship and board tenure (the re-categorised % of INEDs) also increased over time, the change was not statistically significant. From an agency point of view, these developments are a step in the right direction. The same applies to the replacement of family members at the helm of the board with INEDs whose impartiality is beyond reproach. In the broader South African context, Muchemwa et al. (2016) also reported a significant increase in board independence among JSE-listed firms over time. The implications of enhanced board independence, for FFs and NFFs alike, include stability, objectivity and protection from entrenchment and certain business risks (Gornsztein & Likhtman, 2020; IoDSA, 2016).

The level of board independence reported by the FFs was consistently and significantly higher than the authors' re-categorisation based on family association and tenure (45.25% vs. 32.39% on average; F[16 924] = 2.78, p ≤ 0.01). The large and growing gap might be because of the shift from using a factual independence approach to categorise INEDs (King III) to a perceptual independence approach (King IV). Shareholder activists who use a strict (factual) definition of independence, might indeed be concerned that the average FF did not meet the King requirement of having a majority of INEDs on the board. They should, however, note that independence is not only influenced by tenure but also by factors such as board dynamics and relationships. The SEW theory in particular highlights the presence of 'binding social ties' in FFs. This term is used to describe the relationships experienced not only among family members but also with other stakeholders, that foster a sense of loyalty and belonging within these firms (Berrone et al., 2012). Attention should also be given to the skills and social capital that long-tenured INEDs bring to the table. Social capital refers to the gain of goodwill and resources through trusting relationships (Arregle et al., 2007). Anecdotal evidence suggests that long tenured INEDs actually have more confidence to challenge executives than their less experienced (i.e., shorter-tenured) counterparts. Long-tenured INEDs serving on FF boards might also aid in resolving conflicts of interest, planning for continuity and enhance accountability.

To avoid shareholder ire, FFs should ensure that sufficient information is disclosed on the processes used to appoint family members to the board. The following example illustrates the point: In 2005, the food retailer Shoprite Holdings was accused of nepotism when second generation family members Adrian Basson and Jacob Wiese were nominated and elected as alternate directors. Whereas some shareholders expressed discontent on independence grounds, others simply wanted to see the nominees' CVs (curricula vitae) to gauge their suitability (Brand, 2005, p. 1). Although shareholder concern is warranted on the basis of director independence and suitable experience, these family directors may be regarded as stewards that had a vested interest in the financial success and continuity of the firm. The appointment of Adrian Basson and Jacob Wiese may thus be argued to have been for the betterment of all shareholder interests.

Assore, a mining holding company, is a good illustration of a JSE-listed FF that proactively addressed shareholders' concerns regarding the independence of their board chair, Desmond Sacco, in 2017. Desmond joined his father Guido in the FF and was appointed to the board in 1974 (as executive). He became board chair in 1992 and held this position until 2017 when the firm delisted from the JSE. The following statement appeared in the firm's integrated report:

Since the chairman represents the controlling shareholder, and to enhance the balance of power and authority on the board, the chairman does not have a casting vote. Additionally, the board has appointed a lead independent director, who also occupies the position of deputy chairman. (Assore, 2017, p. 34)

From an agency perspective, there are several reasons to have a lead independent director which include the enhancement of managerial monitoring and increased consideration of minority shareholder interests (Bonazzi & Islam, 2017; Muniandy & Hullier, 2015).

The PSG Group also assured shareholders that the independence of long-tenured INEDs and factors that could potentially impair their objectivity were evaluated on an ongoing basis. In their 2022 integrated report, this investment holding company stated:

The board is satisfied with the independence of all the non-executive directors classified as being independent, including Messrs ZL Combi, PE Burton and CA Otto (one of the founders), who have served on the board for more than 10 years. These individuals have a thorough understanding and valuable knowledge of PSG Group's business and associated risks, and always act in the best interest of all stakeholders. (PSG Group, 2022, p. 28)

This statement, once again, alludes to the value FFs place on social capital.

In the Grindrod's case, the nomination and governance committee evaluated the independence of all INEDs on a substance-over-form basis, in accordance with King IV. In 2022, Walter Grindrod was not deemed to be independent given that he was an associate of Grindrod Investments (Pty) Ltd which had an 11.02% shareholding in the FF (Grindrod, 2022). Less convincing arguments were presented by other FFs that categorised family members as INEDs. AVI, for example, only stated that:

The board assessed the independence of Gavin Tipper, James Hersov, Mike Bosman and Abe Thebyane, who each have served on the board for more than nine years and was satisfied that each non-executive director acts with independence of mind and in the best interests of the company, fulfil the requirements of King IV in regard to being considered as independent. (AVI, 2022, p. 68)

At the time, James Hersov, a third-generation family member, had a board tenure of 28 years.

In 2022, The Foschini Group reported that six of their nine INEDs had served a term in excess of 9 years:

The Supervisory Board reviewed the independence of Mr M Lewis, Prof. F Abrahams, Ms NV Simamane, Mr E Oblowitz, Mr R Stein and Ms BLM Makgabo-Fiskerstrand (during the relevant meeting the directors recused themselves). After due consideration, the Supervisory Board concluded that the length of their association with the Group does not impair their independence. (The Foschini Group, 2022, p. 64)

At the end of the 2022 financial year, Lewis had been a board member of his family's retail empire for 34 years. Probing questions from shareholder activists regarding the categorisations of Hersov and Lewis as INEDs are warranted given the FFs' vague justifications. The insistence of board independence by shareholder activists is rooted in the agency theory, as minority shareholders wish to protect their interests through sufficient managerial oversight (Kilincarslan, 2021).

As illustrated in Table 4, both gender and race diversity increased significantly over the research period (% of women: F[16 444] = 6.50, p ≤ 0.01 and % of persons of colour [PoC] F[16 444] = 5.16, p ≤ 0.01). Prior research shows that board oversight generally improves with the appointment of more diverse individuals (Arayakarnkul et al., 2022; Ghafoor et al., 2019; Guest, 2019). Shareholders evaluating FF governance from agency and SEW perspectives will thus be pleased with this development. Of the 70 directors representing founding families in the sample, only 5 were women.

Some FFs recognised the importance of transparent reporting to avoid public criticism. In 2012, Famous Brands, for example, reported that their board does not meet the independence criteria of King III as it mainly comprised of founding shareholders and long-serving directors. They stated:

We believe the individual members apply their minds independently, comply with the Companies Act (No. 71 of 2008) and act in the interests of all shareholders motivated also by their personal shareholdings in the company. Their leadership, wise counsel and in-depth knowledge are all attributes that add value to the deliberations of the board. (Famous Brands, 2022, p. 24)

A prominent business journalist in South Africa also demonstrated the importance of the founding family's commitment and experience to ensure the success of the FF. In his tribute to Neil and Cecil Jowell upon their retirement from Trencor's board in 2015, he wrote:

I don't think one can really give enough credit to the Jowells for keeping Trencor relevant for over six decades as the business environment changed, and for calmly overcoming the odd setback. (Trencor, 2015)

In line with the stewardship theory, reference is also made to the skilful manner in which Murray Grindrod chaired the freight solutions firm bearing his name for two decades. Over this period, his freight business grew from a relatively small undertaking to a successful multinational firm. According to the stewardship theory, independent directors are not a necessity as managers are believed to act altruistically for the collective good of the business (Jasir et al., 2023). This theory may be aligned to the SEW theory, as family directors or managers may act as stewards given their commitment to pass their firms down to future generations.

Conclusions and recommendations

This research was the first of its kind to investigate the board composition of JSE-listed FFs with the aim of determining alignment with governance codes and international best practices. The findings show that fewer FFs had family chairs and CEOs at the end of the research period (2022) than at the beginning (2006). They also appointed more INEDs, women and persons of mixed race to the board over the considered period. In line with King IV recommendations of increased board independence and diversity, this result is welcome as it may lead to improved managerial oversight (IoDSA, 2016). Many of the directors who were categorised as INEDs were, however, family members and had tenures of more than 9 years. Some FFs justified these appointments by explaining how these directors' impartiality was assessed. Reporting at other FFs left much to be desired. The lack of transparency in reporting may signal that the primary interest in FFs is preserving their SEW instead of considering the interests of all shareholders (both family and minority). Probing questions from shareholder activists on this topic is thus warranted.

To avoid raising shareholders' ire, nomination committees of JSE-listed FFs should improve disclosure on the topic of board independence. Where INEDs are family members, more focus should be placed on the value of family involvement and commitment as captured in the stewardship theory. The authors concur with Gornsztein and Likhtman's (2020, p. 2) suggestion that nomination committees should place more emphasis on 'genuine independence, diversity and inclusion'. While difficult to measure, nomination committees should attempt to assess the psychological capabilities, emotional intelligence and experience of INEDs to effectively question long-held assumptions, reduce the risk of groupthink and stimulate innovation. Attention should be given to the number of board positions held concurrently, interactions during and outside of board meetings, and each INEDs relationship with the CEO, the workforce, and investors. Where possible, the quality of independent thought should also be examined (Gornsztein & Likhtman's 2020). A board culture should be created, which gives family and non-family directors the confidence to challenge management and create discomfort, if necessary.

Family firms need to deliver on promises of board refreshment and succession planning. When appointing chairs, care should be taken to ensure that these individuals are able to provide the traditional functions of financial and governance oversight while ensuring that their firms meet society's expectations regarding purpose, diversity, equity and inclusion. Clear and comprehensive communication is critical in cases where the family is perceived to preserve their SEW at all costs. Family firms are likely to experience more public criticism if they continue to disregard independence and disclosure best practices.

Activists should, however, notice that public disclosures offer a limited perspective on the quality of FF governance. They would also do well to heed Lane et al.'s (2006) warning:

Fixating on issues such as board independence tends to overshadow the issue that is at the heart of corporate governance problems around the globe: accountability. Accountability refers to the need for decision makers to justify and accept responsibility for decisions taken and their implementation. Corporate governance guidelines for FFs, therefore, must focus on the need for the board to have the competencies to hold others accountable, and be held accountable, for their actions. (p. 48)

Dedicated and continuous engagements between boards and investors who care about board composition and governance will offer valuable insights on efforts to reduce agency costs. Non-family directors are urged to develop their own sources of information to supplement board packs. In doing so, the information imbalance between themselves and family directors and managers could be properly addressed. Additional insights would also assist in identifying activities by the family to preserve their SEW, such as appointing family managers rather than more experienced non-family managers or overlooking poor decision-making of family managers and/or directors because of the emotional attachment of family members (Berrone et al., 2012). Policy makers such as the King Committee, JSE and IoDSA are encouraged to offer more director and investor training on the topic of FF governance. The unique contributions of family stewards might call for a more nuanced approach to governance requirements. Newly elected INEDs should recognise that there are important differences in governance between FFs and non-FFs. While critical enquiry is equally important in both types of firms, INEDs are likely to experience more ideological tensions in paternalistically run FFs than their counterparts in other types of firms.

The main limitation of this study relates to the exclusion of alternate directors, some of which were family members. Future studies could perhaps include these directors and investigate skills gaps present on FF boards. Specific attention should be given to cybersecurity and climate change. Family Firm boards that are able to combine deep relevant experience and knowledge with independence will be better positioned to create lasting value for all their shareholders and stakeholders. Attention could also be given to the number of boards on which the FFs' INEDs serve concurrently. While multi-boarded directors bring a great deal of experience to the table, they might also be too busy to fulfil their monitoring roles effectively. Focus should be placed on the number of board positions held concurrently, interactions during and outside of board meetings, and relationships with the FF's CEO, workforce and investors. In light of increased incidences of CV fraud in South Africa, more stringent verification processes are also recommended.

While every effort was taken to identify family members based on surnames, future studies could further refine the database to determine the true extent of family involvement, particularly at FFs that have been in existence for a few generations. Qualitative researchers could investigate interactions between directors during and outside of board meetings, and how culture influences boardroom dynamics at FFs. Future researchers could also develop a governance index for FFs and NNFs, and use these indices to examine differences in terms of financial performance and other governance outcomes such as an ethical culture, good performance, effective control and legitimacy.

Acknowledgements

The authors wish to thank Prof. Christo Boshoff and Stellenbosch University for financial support to complete this research. A word of gratitude is also extended to Prof. Martin Kidd and Mr Emile Terblanche for their assistance with the data collection and analysis. Ms Joy-Marie Lawrence of Boardvisory (Pty) Ltd. provided valuable insights, which enhanced the quality of the conclusions and recommendations as did several delegates at the second Corporate Governance Conference hosted by Stellenbosch Business School. The authors would like to thank these individuals for sharing their knowledge with them.

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this article.

Authors' contributions

S.V. supervised the study, conceptualised the article, collected some of the data and wrote the first draft. G.d.S. collected some of the data, assisted with the analysis, wrote some sections, reviewed and edited the article. G.d.S. was also responsible for funding acquisition and project administration. E.V. supervised the study, assisted with the formal analysis and validation. E.V. also reviewed and edited the article.

Ethical considerations

Ethical approval to conduct this study was obtained from the Stellenbosch University Research Ethics Committee: Social Behavioural and Education Research. (No. ONB-2023-27644)

Funding information

Funding was provided by Stellenbosch University through their Postgraduate Scholarship Programme 2023.

Data availability

The data that support the findings of this study are available on request from the corresponding author, S.V.

Disclaimer

The views and opinions expressed in this article are those of the authors and are the product of professional research. The article does not necessarily reflect the official policy or position of any affiliated institution, funder, agency, or that of the publisher. The authors are responsible for this article's results, findings, and content.

References

Acquaah, M., & Eshun, J.P. (2016). Family business research in Africa: An assessment. Family business in Sub-Saharan Africa, 1(1), 43-93. https://doi.org/10.1057/978-1-137-36143-1_3 [ Links ]

Andersson, F.W., Johansson, D., Karlsson, J., Lodefalk, M., & Poldahl, A. (2018). The characteristics of family firms: Exploiting information on ownership, kinship, and governance using total population data. Small Business Economics, 51(3), 539-556. https://doi.org/10.1007/s11187-017-9947-6 [ Links ]

Arayakarnkul, P., Chatjuthamard, P., & Treepongkaruna, S. (2020). Board gender diversity, corporate social commitment and sustainability. Corporate Social Responsibility and Environmental Management, 29(1), 1706-1721. https://doi.org/10.1002/csr.2320 [ Links ]

Aronoff, C., & Ward, J. (2016). More than family: Non-family executives in the family business. Springer.

Arregle, J., Hitt, M.A., Sirmon, D.G., & Very, P. (2007). The development of organisational social capital: Attributes of family firms. Journal of Management Studies, 44(1), 73-95. https://doi.org/10.1111/j.1467-6486.2007.00665.x [ Links ]

Arteaga, R., & Escribá-Esteve, A. (2021). Heterogeneity in family firms: Contextualising the adoption of family governance mechanisms. Journal of Family Business, 11(2), 200-222. https://doi.org/10.1108/JFBM-10-2019-0068 [ Links ]

Assore. (2017). Annual integrated report. Retrieved from https://www.assore-reports.co.za/reports/iar-2017/pdf/full.pdf.

AVI. (2022). Integrated annual report. Retrieved from https://www.avi.co.za/wp-content/uploads/2022/10/Integrated-Annual-Report-June-2022.pdf.

Bendickson, J., Muldoon, J., Liguori, E., & Davis, P.E. (2016). Agency theory: The times, they are a-changin'. Management Decision, 54(1), 174-193. https://doi.org/10.1108/MD-02-2015-0058 [ Links ]

Benjamin, S.J., Wasiuzzaman, S., Mokhtarinia, H. & Nejad, N. (2016). Family ownership and dividend payout in Malaysia. International Journal of Managerial Finance, 12(3), 314-334. https://doi.org/10.1108/IJMF-08-2014-0114 [ Links ]

Bhattacharyya, N., Elston, J.A., & Rondi, L. (2014). Executive compensation and agency costs in a family controlled corporate governance structure: The case of Italy. International Journal of Corporate Governance, 5(3), 119-132. https://doi.org/10.1504/IJCG.2014.064727 [ Links ]

Berrone, P., Cruz, C., & Gomez-Mejia, L.R. (2012). Socioemotional wealth in family firms: Theoretical dimensions, assessment approaches, and agenda for future research. Family Business Review, 25(3), 258-279. https://doi.org/10.1177/0894486511435355 [ Links ]

Bonazzi, L., & Islam, S.M.N. (2007). Agency theory and corporate governance: A study of the effectiveness of board in their monitoring of the CEO. Journal of Modeling in Management, 2(1), 7-23. https://doi.org/10.1108/17465660710733022 [ Links ]

Brand, N. (2005). Nepotism at Shoprite?. News24, 30 September. Retrieved from https://www.news24.com/Fin24/Nepotism-at-Shoprite-20050930.

Buthelezi, L. (2018). Simon Susman to end 36-year journey with Woolworths. Business day, 12 November. Retrieved from https://www.businesslive.co.za/bd/companies/retail-and-consumer/2018-11-12-woolworths-chair-simon-susman-to-retire-in-a-year/.

Carney, M., Van Essen, M., Gedajlovic, E.R., & Heugens, P.P.M.A.R. (2015). What do we know about private family firms? A meta-analytical review. Entrepreneurship Theory and Practice, 39(3), 513-544. https://doi.org/10.1111/etap.12054 [ Links ]

Cassim, R. (2022). An analysis of trends in shareholder activism in South Africa. African Journal of International and Comparative Law, 30(2), 149-174. https://doi.org/10.3366/ajicl.2022.0402 [ Links ]

Chrisman, J., Chua, J., Le Breton-Miller, I., Miller, D., & Steier, L. (2018). Governance mechanisms and family firms. Entrepreneurship Theory and Practice, 42(2), 171-186. https://doi.org/10.1177/1042258717748650 [ Links ]

Clarke, T. (2004). Theories of corporate governance. The Philosophical Foundation of Corporate Governance, 12(4), 244-266. https://doi.org/10.1111/j.1467-8683.2004.00395.x [ Links ]

Corbetta, G., & Salvato, C. (2004). The board of directors in family firms: One size fits all?. Family Business Review, 17(2), 119-134. https://doi.org/10.1111/j.1741-6248.2004.00008.x [ Links ]

Crotty, A. (2021). Bell's historic blunder. Business day, 2 December. Retrieved from https://www.businesslive.co.za/fm/money-and-investing/2021-12-02-bells-historic-blunder/#:~:text=Bell%E2%80%99s%20historic%20blunder%20The%20company%E2%80%99s%20widely%20panned%20lowball,in%20a%20victory%20for%20activists%20and%20minority%20investors.

Crotty, A. (2019). Woolworths: How Simon Susman made all the difference. Business Day, 12 December. Retrieved from https://www.businesslive.co.za/fm/money-and-investing/2019-12-12-woolworths-how-simon-susman-made-all-the-difference/.

Curado, C., & Mota, A. (2021). A systematic literature review on sustainability in family firms. Sustainability, 13(7), 1-17. https://doi.org/10.3390/su13073824 [ Links ]

Dah, B.A., Dah, M.A., & Frye, M.B. (2023). Board refreshment: Like a breath of fresh air. British Journal of Management, 35(1), 378-401. https://doi.org/10.1111/1467-8551.12718 [ Links ]

Daspit, J.J., Chrisman, J.J., Ashton, T., & Evangelopoulos, N. (2021). Family firm heterogeneity: A definition, common themes, scholarly progress and directions for future research. Family Business Review, 34(3), 296-322. https://doi.org/10.1177/08944865211008350 [ Links ]

Davids, E., & Kitcat, R. (2023). The shareholder rights and activism review. The Law Reviews. Retrieved from https://bowmanslaw.com/wp-content/uploads/2023/09/South-Africa.pdf.

Dinh, T.Q., & Calabrò, A. (2019). Asian family firms through corporate governance and institutions: A systematic review of the literature and agenda for future research. International Journal of Management Reviews, 21(1), 50-75. https://doi.org/10.1111/ijmr.12176 [ Links ]

Fama, E.F., & Jensen, M.C. (1983). Separation of ownership and control. Journal of Law and Economics, 26(2), 301-325. https://doi.org/10.1086/467037 [ Links ]

Famous Brands. (2022). Integrated annual report. Retrieved from https://famousbrands.co.za/iar2022/pdf/Famous_Brands_IAR_2022.pdf.

Farrington, S.M., Venter, E., & Beck, S.B. (2020). Parental influences on the next generation's intention to join their family business. Journal of Contemporary Management, 17(2), 74-101. https://doi.org/10.35683/jcm19051.65 [ Links ]

Garcia-Meca, E., & Santana-Martin, D.J. (2023). Board gender diversity and performance in family firms: Exploring the faultline of family ties. Review of Managerial Science, 17, 1559-1594. https://doi.org/10.1007/s11846-022-00563-3 [ Links ]

Ghafoor, A., Zainudin, R., & Mahdzan, N.S. (2019). Factors eliciting corporate fraud in emerging markets: Case of firms subject to enforcement actions in Malaysia. Journal of Business Ethics, 160(1), 587-608. https://doi.org/10.1007/s10551-018-3877-3 [ Links ]

Gomez-Mejia, L.R., Cruz, C., Berrone, P., & De Castro, J. (2011). The bind that ties: Socioemotional wealth preservation in family firms. Academy of Management Annals, 5(1), 653-707. https://doi.org/10.5465/19416520.2011.593320 [ Links ]

Gomez-Mejía, L.R., Haynes, K.T., Núñez-Nickel, M., Jacobson, K.J.L. & Moyano-Fuentes, J., 2007, Socioemotional wealth and business risks in family-controlled firms: Evidence from Spanish olive oil mills. Administrative Science Quarterly, 52(1), 106-137. https://doi.org/10.2189/asqu.52.1.106 [ Links ]

Gornsztein, J., & Likhtman, S. (2020). Guiding principles for an effective board. Federated Hermes, April. Retrieved from https://www.hermes-investment.com/uk/en/intermediary?phrase=guiding+principles+for+an+effective+board.

Green, J., & Moodley, T. (2021). Is this a good time to consider delisting from the JSE? CliffDekkerHofmeyer. Retrieved from https://www.cliffedekkerhofmeyr.com/en/news/publications/2020/corporate/corporate-and-commercial-alert-22-april-is-it-a-good-time-to-consider-delisting-from-the-jse.html.

Grindrod. (2022). Integrated annual report. Retrieved from https://grindrod.com/share_holder_documents/document_2501/_GND%202022%20Integrated%20Annual%20Report.pdf.

Guest, P.M. (2019). Does board ethnic diversity impact board monitoring outcomes? British Journal of Management, 30(1), 53-74. https://doi.org/10.1111/1467-8551.12299 [ Links ]

Habib, A., Wu, J., Bhuiyan, B.U., & Sun, X. (2019). Determinants of auditor choice: Review of the empirical literature. International Journal of Auditing, 23(2), 308-335. https://doi.org/10.1111/ijau.12163 [ Links ]

Hasenfuss, M. (2008). Control freaks: Unbearable tightness of being costs shareholders billions. News24, 19 June. Retrieved from https://www.news24.com/Fin24/control-freaks-unbearable-tightness-of-being-costs-shareholders-billions-20080616-2.

Hasenzagl, R., Hatak, I., & Frank, H. (2018). Problematizing socioemotional wealth in family firms: A systems-theoretical reframing. Entrepreneurship and Regional Development, 30(1-2), 199-223. https://doi.org/10.1080/08985626.2017.1401123 [ Links ]

Institute of Directors South Africa (IoDSA). (1994). The King report on corporate governance. Institute of Directors South Africa. Retrieved from https://cdn.ymaws.com/www.iodsa.co.za/resource/collection/94445006-4F18-4335-B7FB-7F5A8B23FB3F/King_1_Report.pdf.

Institute of Directors South Africa (IoDSA). (2002). King II report on corporate governance for South Africa 2002. Institute of Directors South Africa. Retrieved from https://cdn.ymaws.com/www.iodsa.co.za/resource/collection/94445006-4F18-4335-B7FB-7F5A8B23FB3F/IoDSA_King_II_web_version.pdf.

Institute of Directors South Africa (IoDSA). (2009). King III report on corporate governance for South Africa 2009. Institute of Directors South Africa. Retrieved from https://cdn.ymaws.com/www.iodsa.co.za/resource/resmgr/king_iii/King_Report_on_Governance_fo.pdf.

Institute of Directors South Africa (IoDSA). (2016). King IV report on corporate governance for South Africa 2016. Institute of Directors South Africa. Retrieved from https://cdn.ymaws.com/www.iodsa.co.za/resource/collection/684B68A7-B768-465C-8214-E3A007F15A5A/IoDSA_King_IV_Report_-_WebVersion.pdf.

Jasir, M., Khan, N.U., & Barghathi, Y. (2023). Stewardship theory of corporate governance and succession planning in family businesses of UAE: Views of the owners. Qualitative Research in Financial Markets, 15(2), 278-295. https://doi.org/10.1108/QRFM-08-2021-0135 [ Links ]

Jong, L., & Ho, P.-L. (2019). Family directors, independent directors, remuneration committee and executive remuneration in Malaysian listed family firms. Asian Review of Accounting, 28(1), 24-47. https://doi.org/10.1108/ARA-04-2019-0099 [ Links ]

Kang, H.C., & Kim, J. (2016). Why do family firms switch between family CEOs and non-family professional CEO? Evidence from Korean Chaebols. Review of Accounting and Finance, 15(1), 45-64. https://doi.org/10.1108/RAF-03-2015-0032 [ Links ]

Kerai, A., Marzano, R., Piscitello, L., & Singla, C. (2023). The role of founder CEO and independent board in family firms' international growth: Evidence from India and Italy. Cross Cultural and Strategic Management, 30(4), 704-732. https://doi.org/10.1108/CCSM-08-2022-0139 [ Links ]

Khadija, M. (2022). Performance of German family firms: A focus on foundation ownership and board diversity. Unpublished doctoral dissertation, Otto Beisheim School of Management, Germany. [ Links ]

Kilincarslan, E. (2021). The influence of board independence on dividend policy in controlling agency problems in family firms. International Journal of Accounting and Information Management, 29(4), 552-582. https://doi.org/10.1108/IJAIM-03-2021-0056 [ Links ]

Lane, S., Astrachan, J., Keyt, A., & McMillan, K. (2006). Guidelines for family business boards of directors. Family Business Review, 19(2), 147-167. https://doi.org/10.1111/j.1741-6248.2006.00052.x [ Links ]

Madison, K., Holt, D.T., Kellermanns, F.W., & Ranft, A.L. (2016). Viewing family firm behavior and governance through the lens of agency and stewardship theories. Family Business Review, 29(1), 65-93. https://doi.org/10.1177/0894486515594292 [ Links ]

Mandato, J., & Devine, W. (2020). Why the CEO shouldn't also be the board chair. Harvard Business Review, March. Retrieved from https://hbr.org/2020/03/why-the-ceo-shouldnt-also-be-the-board-chair.

Mans-Kemp, M., & Van Zyl, M. (2021). Reflecting on the changing landscape of shareholder activism in South Africa. South African Journal of Economic and Management Sciences, 24(1), a3711. https://doi.org/10.4102/sajems.v24i1.3711 [ Links ]

Marais, J. (2010). Woolies appointment flies in face of King code. Sunday Times, 21 November. Retrieved from https://www.timeslive.co.za/sunday-times/business/2010-11-21-woolies-appointment-flies-in-face-of-king-code/.

Martini, A. (2021). Socially responsible investing: From the ethical origins to the sustainable development framework of the European Union. Environment, Development and Sustainability, 23(1), 16874-16890. https://doi.org/10.1007/s10668-021-01375-3 [ Links ]

Mashele, A. (2021). Corporate governance and performance of JSE listed family firms. Unpublished Master's thesis, University of Johannesburg, South Africa. [ Links ]

Metsola, J., Leppäaho, T., Paavilainen-Mäntymäki, E. & Plakoyiannaki, E. (2020). Process in family business internationalisation: The state of the art and ways forward. International Business Review, 29(2), 101665. https://doi.org/10.1016/j.ibusrev.2020.101665 [ Links ]

Molly, V., & Michiels, A. (2021). Dividend decisions in family businesses: A systematic review and research agenda. Journal of Economic Surveys, 36(1), 992-1026. https://doi.org/10.1111/joes.12460 [ Links ]

Morgan, T.J., & Gomez-Mejia, L.R. (2014). Hooked on a feeling: The affective component of socioemotional wealth in family firms. Journal of Family Business Strategy, 5(3), 280-288. https://doi.org/10.1016/j.jfbs.2014.07.001 [ Links ]

Muchemwa, R., Padia, N., & Callaghan, C.W. (2016). Board composition, board size and financial performance of Johannesburg Stock Exchange companies. South African Journal of Economic and Management Sciences, 19(4), 497-513. https://doi.org/10.4102/sajems.v19i4.1342 [ Links ]

Muniandy, B., & Hillier, J. (2015). Board independence, investment opportunity set and performance of South African firms. Pacific-Basin Finance Journal, 35(1), 108-124. https://doi.org/10.1016/j.pacfin.2014.11.003 [ Links ]

Naldi, L., Cennamo, C., Corbetta, G., & Gomez-Mejia, L. (2013). Preserving socioemotional wealth in family firms: Asset or liability? The moderating role of business context. Entrepreneurship Theory and Practice, 37(6), 1341-1360. https://doi.org/10.1111/etap.12069 [ Links ]

Neckebrouck, J., & Schulze, W. (2018). Are family firms good employers? The Academy of Management Journal, 61(2), 553-585. https://doi.org/10.5465/amj.2016.0765 [ Links ]

Ntim, C.G. (2013). An integrated corporate governance framework and financial performance in South African-listed corporations. South African Journal of Economics, 81(3), 373-392. https://doi.org/10.1111/j.1813-6982.2011.01316.x [ Links ]

PSG Group. (2022). Annual report. Retrieved from https://www.psggroup.co.za/Annual-Report-2022.pdf.

Rabenowitz, P., Botha, M., Rossini, L., Du Preez, L., Geach, W., & Goodall, B. (2018). The South African financial planning handbook. Sage.

Rovelli, P., Ferasso, M., De Massis, A., & Kraus, S. (2021). Thirty years of research in family business journals: Status quo and future directions. Journal of Family Business Strategy, 13(3), 1-17. https://doi.org/10.1016/j.jfbs.2021.100422 [ Links ]

Sageder, M., Mitter, C., & Feldbauer-Durstmüller, B. (2018). Image and reputation of family firms: A systematic literature review of the state of research. Review of Managerial Science, 12(1), 335-377. https://doi.org/10.1007/s11846-016-0216-x [ Links ]

Shaw, T.S., He, L., & Cordeiro, J. (2021). Delayed and decoupled: Family firm compliance with board independence requirements. British Journal of Management, 32(1), 1141-1163. https://doi.org/10.1111/1467-8551.12509 [ Links ]

Sherlock, C., Markin, E., Swab, R.G., & Yates, V.A. (2022). A systematic examination of the family business contributions: Is this domain a legitimate field of research? Journal of Management History, 29(3), 399-422. https://doi.org/10.1108/JMH-08-2022-0031 [ Links ]

Shingade, S., Rastogi, S., Bhimavarapu, V.M., & Chirputkar, A. (2022). Shareholder activism and its impact on profitability, return, and valuation of the firms in India. Journal of Risk and Financial Management, 15(4), 148-168. https://doi.org/10.3390/jrfm15040148 [ Links ]

Robino, F.E., Tenuta, P., & Cambrea, D.R. (2017). Board characteristics effects on performance in family and non-family business: A multi-theoretical approach. Journal of Management and Governance, 21, 623-658. https://doi.org/10.1007/s10997-016-9363-3 [ Links ]

The Foschini Group. (2022). Integrated annual report. Retrieved from https://tfglimited.co.za/wp-content/uploads/2022/08/TFG_Interactive-IAR_2022.pdf.

Trencor. (2015). Integrated annual report. Retrieved from https://trencor.net/wp-content/uploads/2019/01/Jowells_Tribute.pdf.

Venter, E., & Hayidakis, H. (2021). Determinants of innovation and its impact on financial performance in South African family and non-family small and medium-sized enterprises. The Southern African Journal of Entrepreneurship and Small Business Management, 13(1), 1-14. https://doi.org/10.4102/sajesbm.v13i1.414 [ Links ]

Viviers, S. (2022). Assessing the relationship between governance quality and shareholder voting opposition at listed family firms in South Africa. Management Dynamics, 31(1), 18-38. https://hdl.handle.net/10520/ejc-mandyn-v31-n1-a2 [ Links ]

Viviers, S., Mans-Kemp, N., Kallis, L., & Mckenzie, K. (2019). Public 'say on pay' activism in South Africa: Targets, challengers, themes and impact. South African Journal of Economic and Management Sciences, 22(1), a3251. https://doi.org/10.4102/sajems.v22i1.3251 [ Links ]

Yamahaki, C., & Frynas, J.G. (2016). Institutional determinants of private shareholder engagement in Brazil and South Africa: The role of regulation. Corporate Governance: An International Review, 24(5), 509-527. [ Links ]

Correspondence:

Correspondence:

Suzette Viviers

sviviers@sun.ac.za

Received: 07 Mar. 2024

Accepted: 22 July 2024

Published: 27 Aug. 2024

Annexure A

{kind=link}

{kind=link}

{kind=link}