Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

On-line version ISSN 2411-9717Print version ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.125 n.6 Johannesburg Jun. 2025

https://doi.org/10.17159/2411-9717/2826/2025

PROFESSIONAL TECHNICAL AND SCIENTIFIC PAPERS

Guide memoire: The principles of reasonable prospects for eventual economic extraction

T. MapetaI; S.M. RupprechtII

IA & B Global Mining, South Africa

IIUniversity of Johannesburg, South Africa. ORCiD: http://orcid.org/0000-0003-2462-2819

ABSTRACT

Discussions on reasonable prospects for eventual economic extraction (RPEEE) include the CRIRSCO 2019 reporting template, JORC 2012, SAMREC 2016, CIM 2019 Guideline, and Regulation SK-1300. These reporting codes all conform to the principles of reasonable prospects for eventual economic extraction. To demonstrate that all mineral resources align with the RPEEE principles, the Competent Person is responsible for endorsing the mineral resource estimate. Moreover, establishing mineral resources and RPEEE requires technical input from numerous technical specialists, such as mining and geotechnical engineers, metallurgical engineers, social and environmental specialists, financial and governmental practitioners, and more. The aim is to improve the transparency of the disclosure of mineral resources and guarantee the investor or potential investor that the reporting of mineral resources is based on reliable technical, economic, environmental, social, and other relevant factors.

This paper discusses the important protocols and definitions in some international reporting codes for the purposes of developing a guide memoire that will assist the Competent Person to interpret, establish and apply RPEEE appropriately and easily.

Keywords: reasonable prospect for eventual economic extraction (RPEEE), Competent Person, reporting codes, mineral resources

Introduction

The world's main national reporting organisations (NRO), the JORC Code (Australia), the CIM Definition Standards (Canada), the SAMREC Code (South Africa), and other international reporting codes (CRIRSCO-based codes) all conform to the principles of reasonable prospects for eventual economic extraction (RPEEE) as one of the principal criteria for defining a mineral resource. Definitions vary slightly, but the responsibility is undoubtedly on the Competent Person endorsing the mineral resource estimate to demonstrate that all reported mineral resources align with the RPEEE principles. This paper will discuss the important protocols and definitions in some international reporting codes to develop a guide memoire establishing RPEEE that will assist the Competent Person to easily interpret and apply RPEEE correctly. In addition, the paper will consider recent trends in international reporting of mineral resources, such as the Security Exchange Commissions (SEC) Technical Report Summary filings (SK-1300) and the current rise of importance in environmental, social and governance (ESG) when declaring a mineral resource.

Background to reasonable prospect for eventual economic extraction

Once geological data, e.g., geological model, mineralisation model, and estimation domains, have been collected and identified, it does not necessarily convert the exploration result into a mineral resource. The level of confidence in the data generated during mineral exploration and mineral resource development is influenced by quality assurance and quality control (QA/QC), an essential process that is a requirement in the Committee for Mineral Reserves International Reporting Standards (CRIRSCO)-based International Reporting Codes for Mineral Resource estimation and reporting. To enhance the confidence level in the data collected, QA/QC must ensure precise, accurate, representative, and reliable results of the geoscientific knowledge (Gan et al., 2022). With good standards, working procedures, QA/ QC, and management, reliable information can be produced, which is fundamental for estimating a mineral resource.

To classify a deposit as a mineral resource, the Competent Person must establish that RPEEE exists by estimating or interpreting key geological characteristics from specific geological evidence and other technical information (i.e., modifying factors). This requires an analysis based on specific geological evidence and technical inputs to establish RPEEE. This analysis must be conducted to an appropriate standard and, importantly, more exact than required to disclose exploration results. This level of diligence is critical due to the importance investors are likely to place on the mineral resource estimate (SEC, 2018).

Determining a mineral resource is not merely an inventory of all mineralisation drilled or sampled.

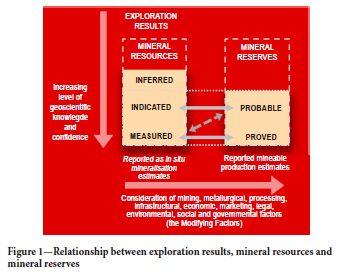

A Mineral Resource is instead a reasonable estimate of mineralisation, taking into account relevant factors such as mining method, cut-off grade, likely mining dimensions, location or continuity, which, with the assumed and justifiable technical and economic conditions, is likely to, in whole or in part, become economically extractable (SAMREC, 2016).

In addition, the Competent Person must consider modifying factors to consider geological information, technical, and economic aspects. The establishment of RPEEE demands an "initial assessment" (preliminary assessment), not simply an inventory of mineralised material above a stated cut-off grade. Although the inputs to estimating the cut-off grade cover some technical and economic aspects, i.e., on- and off-mine costs, recovery and metal price, the cut-off grade doesn't incorporate all relevant factors to establish RPEEE - for example, infrastructure, legal, environmental, social, and governmental inputs.

The authors concur that an initial assessment is sufficient to declare a mineral resource. In the past, some have proposed that a Preliminary Economic Assessment (PEA) or Scoping Study should be the level of evaluation to establish mineral resources. An initial assessment considers the geological and technical factors but doesn't need to go into as much detail as a PEA or Scoping Study. The concept of initial assessment is discussed in more detail further on in this paper.

Unfortunately, for some projects, the establishment of RPEEE falls below the best practice of completing an initial assessment, as incorrect protocols have been implemented. Glacken (2019), in his survey, states that of 37 mineral resource statements reported to the Australian Securities Exchange between May and June 2019, only 11% of the open pit mineral resources statements reported applied an economic pit constraint and that 90% of the underground mineral resources were reported in the absence of any constraint except a cut-off grade. Glacken also found It concerning that the flexibility afforded to Competent Persons in choosing a commodity price for reporting and determining a cut-off grade is sometimes misleading. In some instances, a less than meticulous application was applied when determining RPEEE.

CRIRSCO 2019 reporting template

According to the CRIRSCO International Reporting Template (2019), the term RPEEE implies a judgement (albeit preliminary) by the Competent Person in respect of all modifying factors, which are considered insufficient in technical and economic detail to demonstrate at the time of reporting that extraction is reasonably justified, i.e., a mineral reserve (Anglo American Mineral Resource Report, 2021). In other words, a mineral resource is not an inventory of all mineralisation drilled or sampled (Lock, 2020). It is a realistic inventory of mineralisation, which, under assumed and justifiable technical and economic conditions, may, in whole or in part, become economically extractable (SAMREC, 2016).

Secondly, any material assumptions in determining the RPEEE should be clearly stated, discussed, and justified in the Public Report (CRIRSCO, 2019). Additionally, as preparing a mineral resource estimate is often repetitive, periodically reviewing the assumptions is fundamental as more current and detailed information becomes available (CIM, 2019).

JORC 2012

The Joint Ore Reserves Committee (JORC) was established in 1971; it outlines minimum standards, recommendations, and guidelines for Public Reporting in Australasia of exploration results, mineral resources, and ore reserves. It defines the following (JORC, 2012):

> A mineral resource is a concentration or occurrence of solid material of economic interest in or on the Earth's crust in such form, grade (or quality), and quantity that there are RPEEE.

> A mineral resource must not include portions of a deposit that does not have RPEEE. The basis for the reasonable prospects assumption is always a material matter. The Competent Person must explicitly disclose and discuss it within the Public Report using the criteria listed in Table 1 for guidance. The introduction of the Table 1 declaration in the JORC allows the reader to be aware of the RPEEE constraints, or lack thereof (Glacken, 2019). The reasonable prospects disclosure must also discuss the technical and economic inputs used to estimate the cut-off grade.

> Where untested practices are applied in determining reasonable prospects, the Competent Person in the Public Report must justify using the proposed practices for reporting the mineral resource.

When reviewing the JORC Code (2012), one notes the absence of reference to modify factors, with the JORC Code only referencing Table 1. However, the JORC Code defines the terms 'eventual' and 'reasonable' clearly and concisely.

SAMREC 2016

The SAMREC Code (2016) provides the following guidance to Competent Persons. RPEEE should be demonstrated by applying appropriate consideration of the potential viability of the mineral resources. Such a consideration should include a reasoned assessment of the geological, mining engineering, processing, metallurgical, legal, infrastructural, environmental, marketing, socio-political, and economic assumptions (modifying factors) which, in the opinion of the Competent Person, are likely to influence the prospect of economic extraction. All issues listed in Table 1 of the SAMREC Code, under RPEEE, should be discussed appropriately for the specific investigation. The determination of RPEEE should be based on the principle of reasonableness and should be justifiable and defendable.

CIM 2019 guideline

The Canadian Institute of Mining (CIM) 2019 Mineral Resource and Mineral Reserve Best Practice Guidelines are based on well-established estimation and mine planning principles and are designed to provide general guidance for best professional practices in preparing mineral resource and mineral reserve estimates (CIM, 2019).

Although these guidelines are neither intended to be prescriptive, nor to provide detailed and exhaustive instructions, they are very informative about the requirements to estimate a mineral resource.

The 2019 Mineral Resource and Mineral Reserve Best Practice Guidelines focus on geological aspects and include other areas to be considered, like factors significant to potential technical feasibility and economic viability. These factors consist of such items as:

> The size and legal conditions of the land tenure; is it sufficient to support the declaration of a mineral resource.

> The extraction selectivity for the mining methods under consideration relative to the size and geometries of the interpreted mineralisation.

> The processing method under consideration, the expected recovery from the mineralised material to a commercially marketable product, and the proposed production volume.

> The price/value of the product and the market for the product at that price.

> The factors significant to cut-off grades or values (e.g., process recovery, smelter payability, treatment charges, operating costs, royalties, and metal price) used for reporting the mineral resource estimates.

> Developing a conceptual operating scenario should be considered early in the mineral resource estimation process. This initial view is formed by Competent Persons based on their judgement and experience. This initial conceptual operating scenario may evolve as new information becomes available. The guideline stresses the use of consultation with colleagues, i.e., technical specialists.

The level of work (initial assessment) to support the declaration of a mineral resource should not be regarded as a scoping study. Still, an initial assessment promotes the requirement to investigate beyond just geology and highlights that mineral resources require inputs from other technical specialists and consideration of the modifying factors.

Regulation SK-1300

The United States Security Exchange Commission (SEC) proposed a revision to its disclosure requirements in June 2016. The amendments aim to provide investors with a broader understanding of a registrant's mining properties, which should assist investors in making more informed investment decisions (Rupprecht, 2020). The following points summarise the revision:

> Reasonable prospects of economic extraction based on initial assessment:

• The SEC believes that reasonable prospects for economic extraction will occur over a timeline. Thus, the requirement of 'eventual" is removed from RPEEE, and instead, reasonable prospects of economic extraction are required. This means that reasonable prospects for a mineral resource's economic extraction do not require the extraction to occur immediately. Rather, one would expect it to occur over a temporal period, which will vary depending on the mineral or commodity being mined.

• Requires a qualified person to apply relevant technical and economic factors likely to influence the prospect of economic extraction, rather than all modifying factors, when determining mineral resources.

Initial asssessment (also a scoping study)

The SEC (SK-1300) proposes that a registrant's disclosure of mineral resources must be based upon a qualified person's "initial assessment" supporting the determination of mineral resources. The SK-1300 regulation defines an "initial assessment" as a preliminary technical and economic study of the economic potential of all or parts of mineralisation to support the disclosure of mineral resources. This requirement is more onerous than the international reporting codes, as the S-K 1300's initial assessment represents the equivalent of a scoping Study, which is above the level of study required by the CRIRSCO-based codes.

The initial assessment must be prepared and justified by a qualified person. It must include appropriate assessments of reasonably assumed modifying factors and any other relevant operational factors necessary to demonstrate that there are reasonable prospects for economic extraction at the time of reporting. When reporting a mineral resource, the Competent Person should try to identify mineralised material that has "reasonable prospects" but may not be a mineral reserve (Gossan, Smith, 2007)).

SK1300 - commentary

The SK-1300 regulation requires a qualified person to apply relevant technical and economic factors likely to influence the reasonable prospect of economic extraction. An initial assessment considering all the modifying factors should be conducted to determine a mineral resource.

It may be beneficial for the International Reporting Codes to adopt the requirement of an initial assessment to support the declaration of the mineral resource estimate. However, further guidance is required to define initial assessment as a technical study that is less than the requirements of a PEA or Scoping Study (Unlike the definition used in the SK-1300 regulations).

SK-1300 definition leaves out eventual

Previously mining property disclosures were reported in accordance with the requirements of the SEC's Industry Guide 7. On October 31, 2018, the SEC adopted amendments to modernise the property disclosure requirements for mining registrants. The amendments consolidate the SEC's mining property disclosure requirements by relocating them to a new subpart of Regulation SK-1300 (Subpart 1300) (SK-1300).

SK-1300 applies to all mining (hard rock and brine) and royalty companies listed on the US stock exchange. The SK-1300 amendments aim to ensure investors know how to make informed decisions about material mining properties (Parson, Sullivan, 2019).

Notably, the SK-1300 definition leaves out 'eventual' from the RPEEE classification. The important question is though: Should the International Reporting Codes also consider omitting it without losing the significance and meaning of the RPEEE protocol? As stated in SEC (2018):

...one expects that reasonable prospects for a Mineral Resource's economic extraction will occur over a temporal period, depending on the mineral or commodity being mined. Under the final rules, the Qualified Person will choose the appropriate period when determining whether mineral resources exist and, if the property is material, must explain its choice in the technical report summary.

General discussion

The phrase 'reasonable prospects for eventual economic extraction' suggests an initial assessment by the Competent Person regarding all matters likely to influence the prospect of economic extraction, including the approximate mining parameters. Considering the parameters, the principle should be reasonable (not conservative or overly optimistic). The Competent Person estimating the mineral resource should attempt to identify and consider all material aspects that impact RPEEE (Gosson, Smith, 2007).

Importantly, a mineral resource is not just an inventory of all mineralisation drilled or sampled. It is a realistic inventory of mineralisation which, under assumed and justifiable technical, economic, and development conditions, might, in whole or in part, become economically extractable. The economic potential requirement is often demonstrated by selecting an appropriate cut-off grade (or value). "A time-honoured concept that remains unchanged" (Pressacco et al., 2021).

Interpreting 'eventual' in this context may differ depending on the commodity or mineral (Lock, 2020). For instance, for some minerals or commodities, it may be reasonable to predict 'eventual economic extraction' as covering over 50 years. Yet, for most smaller deposits, the application of the concept would normally be limited to much shorter periods. In all cases, the Competent Person should disclose and discuss the considered time frame.

Others could argue that the word 'eventual' in the RPEEE definition is redundant and could be omitted, as in the SK-1300 Regulation. The reason is that every mineral resource may not be mined immediately but at a particular time when it is economic or when conditions are most favourable. Hence, the term 'eventual' stands for every commodity under assessment.

The importance of ESG for mineral reporting

The environmental, social and governance (ESG) issues have become relevant due to the increasing global awareness of human impacts on our planet.

Under the SAMREC Code, ESG issues are considered a fundamental contributor to modifying factors that play an important role in determining the RPEEE for mineral resources. Investors want to understand how companies integrate ESG aspects into their businesses, and this evidence needs to impact all aspects of the business, including geological processes and activities. However, more and more investors have noted an increasing dissatisfaction with the ESG information presented by companies (Steele-Schober, 2021). A number of companies have been scrutinised for their ESG position, for example, Glencore is being questioned for their long-term commitment to coal (Burton, 2023).

The South African guideline for reporting environmental, social, and governance parameters (SAMESG Guideline) supports the SAMCODES by providing information for authors of public reports on applying the ESG considerations throughout the geological reporting process (SAMESG Committee, 2017).

Definitions

In the SAMREC Code (2016), the guidelines highlight the consideration of modifying factors and elaborate on the terms 'reasonable' and 'eventual.

The assumptions used to test for 'reasonable prospects' should be even-handed and within known/assumed tolerances or have examples of precedence. These assumptions should be applied at an appropriate scale and may differ from those used for determining mineral reserves and should be appropriate to the definition of mineral resources in terms of precision, accuracy, degree of confidence, and variability. Where untested practices are applied in the determination of 'reasonable prospects, the use of the proposed practices for reporting the mineral resource should be justified by the Competent Person in the Public Report. Interpreting the word 'eventual' in this context of RPEEE may vary depending on the commodity, mineral involved, or legal tenure. For example, for many occurrences of coal, iron ore, bauxite, and other bulk minerals or commodities, it may be reasonable to envisage a life of mine of 50 years or more. However, for other deposits, application of the concept may be restricted to a life of mine of perhaps 20 to 30 years and frequently much shorter periods.

To define 'eventual, the Competent Person might consider the following questions: What will the resource metal price be 30 years from now? Will there be adequate infrastructure to support the project? How will power be generated? Are there any social or environmental issues that could impede the extraction of the mineralised material? The Competent Person has to deal with such questions, even at an early stage of the process (Dixon, n.d.).

Although the CRIRSCO-based international reporting codes use "eventual", it is notable that the SK-1300 regulation has chosen to remove "eventual" from RPEEE. The SK-1300 regulation excludes "eventual" as it expects a

qualified person to consider relevant technical and economic factors likely to influence the prospect of economic extraction, including the pricing for the resource that could be based on forward-looking price forecasts, when determining whether mineral resources exist. [The SK-1300 regulation] believes it is clear from the definition of mineral resource that the reasonable prospects for economic extract will occur over a timeline.

The SK-1300 regulation allows the qualified person to choose the appropriate period when determining whether mineral resources exist and must explain the choice in the technical report summary.

Finally, a 'mineral resource' is a concentration or occurrence of material of economic interest in or on the Earth's crust in such form, quality, and quantity that there are RPEEE. A mineral resource's location, quantity, grade, continuity, and other geological characteristics are known, estimated or interpreted from specific geological evidence and knowledge. Mineral resources are subdivided, in order of increasing geological confidence, into Inferred, Indicated and Measured categories (Dixon, 2022).

Initial assessment

As determined by the SK-1300 regulation, an initial assessment requires an initial assessment for mineral resource disclosure. An "initial assessment" should be viewed as a preliminary technical and economic study of the economic potential of all or parts of mineralisation to support the disclosure of mineral resources. At the time of reporting, the initial assessment must assess the modifying factors and any other material factors necessary to demonstrate RPEEE and the reporting of mineral resources. A key premise of the initial assessment is that it is neither a scoping study nor a PEA; but is solely used to support the disclosure of a mineral resource and not to determine whether to proceed with further work leading to the preparation of a prefeasibility study (SEC, 2018).

Best practice guidelines

Based on the protocols and definitions discussed in the aforementioned section, this paper provides the best guidelines for the Competent Person to determine and report on RPEEE. These guidelines aim to provide guidance and clarity for Competent Persons determining RPEEE and represent the best current reporting practice knowledge. The guidelines are motivated by the desire to provide the industry with technical practices to aid the understanding and implementation of RPEEE.

Role of the Competent Person

The Competent Person declaring mineral resources is typically a mineral resource estimations specialist with a geology background. However, this may not always be the case. When determining RPEEE and estimating mineral resources, the Competent Person relies on geoscientific knowledge to report the in situ mineralisation estimate. Historically, RPEEE may have been determined by the Competent Person alone by applying a cut-off grade. However, over time the determination of RPEEE requires the consideration of the modifying factors, albeit on a high level. This implies that the determination of the mineral resource requires the Competent Person to rely on technical specialists to guide the consideration of the modifying factors. Noting that the Competent Person should demonstrate RPEEE by applying the appropriate modifying factors to establish the potential viability of mineral resources (SAMREC, 2016). Furthermore, the Competent Person must discuss on an if-not-why-not basis all of the RPEEE considerations listed in Table 1 at the level appropriate for the specific investigation (SAMREC, 2016).

Site visit

Site visits are a requirement to be undertaken by a Competent Person. This is, without a doubt, best practice and assists the Competent Person in fully appreciating the technical expectations of the assignment. There are numerous examples where mineral resources or RPEEE were determined only to discover later that infrastructure, ownership, or environmental issues eliminated the prospects of developing the mineral property. For example, a large township situated over a near surface deposit and an international power line located in the centre of a proposed open pit - both situations that negated RPEEE.

Determining cut-off grade for RPEEE

The Competent Person's estimated cut-off grade is based on assumed costs for surface or underground operations, metallurgical recoveries, and commodity prices based on a reasonable basis.

Estimating a cut-off grade is important and utilises several technical factors to estimate the cut-off grade. However, RPEEE rely on more than just a cut-off grade. Other factors must also be considered.

The authors concur that determining the cut-off grade is an important consideration in establishing a mineral resource, and best practice demands that technical specialists are used to providing technical inputs to the cut-off estimation. Nevertheless, in conjunction with other technical specialists, the Competent Person must consider the other modifying factors to establish RPEEE.

Investors must realise that the cut-off grade estimation for RPEEE is preliminary. As further information is gathered, i.e., variations of rock characteristics, mining methods, metallurgical and processing methods, etc., the mineral resource model may necessitate more than one cut-off grade for different deposit areas.

The Competent Person must be transparent when reporting all the inputs used to estimate the cut-off grade used to determine RPEEE, i.e., the mineral resource.

Applying modifying factors to support RPEEE

When determining the existence of a mineral resource, the Competent Person must conclude that there are RPEEE based on an initial assessment that the Competent Person should conduct by qualitatively applying the modifying factors and other relevant technical and economic factors. Best practice would require technical specialists in the specific areas to provide the Competent Person with insight into factors used to establish the RPEEE. The authors would contend that the days of estimating mineral resources solely by a single Competent Person are gone. Investors are entitled to the mineral resource being potentially viable and that all modifying factors have been properly and thoroughly considered.

The modifying factors to be considered during the initial assessment are as follows:

> Mining

> Metallurgical

> Processing

> Economic

> Marketing

> Legal

> Infrastructure

> Environmental

> Social

> Governmental.

Mining

A mining method should be considered before building the geological model and grade tonnage estimate. The mineral resource geologist should obtain the assistance of a mining engineer to determine the mining method and technical implications of such mining method and equipment selection. Establishing a reasonable estimate of the mining method and associated costs is critical in determining the cut-off grade and establishing RPEEE.

For surface mining, understanding geotechnical and hydrological data will determine the slope inclination; they, in turn, will inform the outline of the pit shell and influence the stripping ratio and cost of mining.

Underground mining methods may be more difficult to determine, especially for inferred mineral resources, where the geological information may be limited. The resource geologist must appreciate that the changes to the geology, structure, dip, thickness, and volume of mineralisation, etc., of the deposit can impact the mining method, hence mining operating costs.

The more effort spent considering the mining aspects, the more robust the estimation of RPEEE.

Metallurgical and processing

Including metallurgical test work during the exploration, the process must be considered necessary to enable the Competent Person to determine a mineral resource. Assumptions based on neighbouring operations are poor practice. Just as determining the density of the mineralised material is critical in mineral resource estimations, so too should the determination of the recovery be conducted, if only preliminary.

Infrastructure

Infrastructure can be important in determining RPEEE. Certain infrastructure aspects may be a fatal flaw in establishing a mineral resource. Accessibility of port infrastructure, cost of access to deposit, haulage roads, and the availability of power and water must be considered. Again, the assistance of the technical specialist will ensure incorrect assumptions are not made when trying to establish RPEEE.

Economic and marketing

Based on forward-looking pricing forecasts, when estimating mineral prices, the Competent Person must use a price assumption that is current as of the end of the registrant's most recently completed fiscal year, for each commodity that provides a reasonable and justifiable basis for establishing the prospects for economic extraction of mineral resources.

The practice of omitting commodity prices and/or costs from a public report is no longer the best practice. Recent guidelines, such as the SK-1300, require price and cost disclosure as a foundation for good reporting practices. A description of the methodology used to determine the prices and/or costs should be disclosed. Such disclosure should be in a form that helps the investor to form an opinion of the prices and/or costs used, and whether the inputs are reasonable views of future prices and/or costs.

Legal

The legal status of the property must be investigated. The resource geologist cannot assume that legal aspects are complete. A documentation review is essential to ensure no servitudes or other existing impairments. The authors have seen projects negatively impacted due to not having the mining right to the property, the mineral resource materially reduced due to an infrastructural servitude through the centre of the project, or access to the mineralisation denied due to previous military operations, i.e., deposit located on a defunct artillery range.

Environmental, social, and governmental

Environmental, social, and governmental (governance) (ESG) issues have become paramount over the past few years. In a survey conducted by CRIRSCO, 90% of respondents (national reporting organisations (NROs) that responded), agreed that modifications to existing and new definitions are required to provide clarity on ESG and to accommodate increased ESG integration (SAIMM, 2020).

Technical reports should include, among other matters: the results of environmental studies, such as environmental baseline studies or impact assessments; requirements and plans for waste and tailings disposal; project permitting requirements; plans, negotiations, and agreements with local individuals or groups; and mine closure plans, including remediation and reclamation plans, and the associated costs. The technical report must also include the Competent Person's opinion on the adequacy of current plans to address any issues related to environmental compliance, social and community issues, and permitting and legal compliance.

Mine reclamation and closure

A Competent Person should consider mine reclamation and closure plans when conducting an initial assessment. In addition, when considering RPEEE the Competent Person needs to be confident that no concerns related to closure are present that could prevent the project from being developed.

Mineral resource statements

Regardless of the approach or procedures, the Competent Person must ensure that all mineral resource statements satisfy the RPEEE requirement.

Preparing a geologically sound interpretation that honours the sample data and the controls on mineralisation is an important activity when preparing a mineral resource estimate.

For mineral resources amenable to open pit mining methods, RPEEE should consider not only an economic limit (such as the cut-off grade or value) but technical requirements (such as slope angles). At a minimum, the constraints can be addressed by creating constraining surfaces (pit shells) using commercial software packages or manual methods. The constraining surfaces can then be used with other criteria to determine RPEEE and prepare mineral resource statements.

Best practice includes identifying and ranking risks associated with each input of the mineral resource estimate. Any material assumptions made in determining RPEEE should be clearly stated, discussed, and justified in the technical report.

Conclusion and recommendations

The JORC Code, the CIM Definition Standards, the SAMREC Code, and other International Reporting Codes refer to the principles of RPEEE as one of the essential criteria for defining a mineral resource. The Competent Person is responsible for demonstrating that all mineral resources align with the RPEEE principles. This isn't always the case, with some mineral resource declarations failing to provide sufficient information to support RPEEE.

Notably, the CRIRSCO template and the international reporting codes1 support the consideration of modifying factors to establish RPEEE. A scoping study is:

... an order of magnitude technical and economic study of the potential viability of mineral resources that includes appropriate assessments of realistically assumed modifying factors together with any other relevant operational factors that are necessary to demonstrate at the time of reporting that progress to a Pre-Feasibility Study can be reasonably justified.

The SK-1300 regulation requires an 'initial assessment' for determining mineral resources. Although the SK-1300's definition of an initial assessment is nebulous, its final rule equates an initial assessment to a PEA/scoping study closely resembling an NI-43-101F1 technical report (SEC, 2018). An initial assessment is associated with an accuracy of 50%, which is less accurate than most scoping studies, which have an associated accuracy of ~30% to 50% (Rupprecht, 2004); ~25% to 50% (CRIRSCO, 2019); +35% OPEX and +50% CAPEX (SME, 2017).

The guide memoire for disclosing RPEEE is intended to make it possible for the Competent Person to consider all relevant factors. The authors contend that the declaration of mineral resources requires an initial assessment of the relevant technical and economic factors, i.e., modifying factors that are likely to influence the reasonable prospects of (eventual) economic extraction; noting that an initial assessment cannot be used as the basis for disclosing mineral reserves (SEC, 2018). Although the initial assessment is preliminary, the Competent Person, in association with other technical specialists, must consider all the modifying factors.

The concept that mineral resource reporting is solely the responsibility of the Mineral Resource Geologist is no longer valid. Establishing mineral resources and RPEEE requires technical input from numerous role players, such as mining and geotechnical engineers, metallurgical engineers, social and environmental specialists, financial and governmental practitioners; noting that this list is not exhaustive.

The CRIRSCO-based international reporting codes should consider the migration of RPEEE to include initial assessments. These initial assessments do not need to be long or onerous but should contain sufficient detail to demonstrate that all modifying factors have been adequately considered.

The basis of this recommendation is to improve the transparency of the disclosure of mineral resources and provide the investor with greater assurance that the reporting of mineral resources is based on reliable technical, economic, environmental, social, and other relevant factors.

References

Anglo American plc. 2021. Ore reserves and Mineral Resources Report. 2021. https://www.angloamerican.com/~/media/Files/A/Anglo-American-Group-v5/PLC/investors/annual-reporting/2022/aa-ore-reserves-and-mineral-resources-report-2021.pdf [accessed 08 November 2022]. [ Links ]

Burton, M. 2023. Big investors ask Glencore to justify thermal coal development. https://www.reuters.com/business/sustainable-business/big-investors-ask-glencore-justify-thermal-coal-development-2023-01-05 [accessed 01 May 2023]. [ Links ]

CIM Mineral Resource & Mineral Reserve Committee. 2019. CIM Estimation of Mineral Resources and Mineral Reserves Best Practice Guidelines. https://mrmr.cim.org/en/best-practices/estimation-of-mineral-resources-mineral-reserves [accessed 07 December 2022]. [ Links ]

Committee for Mineral Reserves International Reporting Standards (CRIRSCO). 2019. International Reporting Template for the public reporting of Exploration Results, Mineral Resources and Mineral Reserves. Committee for Mineral Reserves International Reporting Standards, Council of Mining and Metallurgical Institutions (CMMI). [ Links ]

Dixon, R. Reasonable Prospects for Eventual Economic Extraction. SRK News Issue Mineral Resource Estimation. https://www.srk.com/en/publications/reasonable-prospects-for-eventual-economic-extraction-rpeee [accessed 12 November 2022]. [ Links ]

Gan, S., Birrell, L., Robbertze, D., Zhao, B., Van Niekerk, E., Ncubi, L. 2022. Quality control in tailings resource exploration at Havelock Mine, Eswatini. Journal of the Southern African Institute of Mining and Metallurgy, vol. 122, no. 7, pp. 347-62. https://mrmr.cim.org/en/best-practices/estimation-of-mineral-resources-mineral-reserves [ Links ]

Glacken, I.M. 2019. The highly vexed issue of reasonable prospects for eventual economic extraction (RPEEE) narrowing the range of practice. Proceedings Mining Geology 2019, pp. 2635. [ Links ]

Gossan, G., Smith, L. 2007. Reasonable Prospects for Economic Extraction. Canadian Institute of Mining, Metallurgy and Petroleum, Montreal. https://mrmr.cim.org/en/library/magazine-articles/reasonable-prospects-for-economic-extraction [accessed 10 November 2022]. [ Links ]

JORC. 2012. Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (The JORC Code), JORC, Carlton South. [ Links ]

Lock, N. 2020. RPEEE (Reasonable Prospects for Eventual Economic Extraction): The critical core to the SAMREC Code. 2020. The Southern African Institute of Mining and Metallurgy, vol. 120, no. 12, p 498. [ Links ]

Mineral Resources and Mineral Reserves (The SAMREC Code). 2016. The South African Code for The Reporting of Exploration Results. https://www.samcode.co.za [accessed 07 December 2022]. [ Links ]

Parson, B., Sullivan, M. 2019. Investment Implications of The U.S. SEC's Rule S-K 1300. https://www.srk.com/en/publications/investment-implications-of-the-us-secs-rule-s-k-1300 [accessed 08 November 2022]. [ Links ]

Pressacco, R., Evans. L., Postle, J. 2021. Reasonable Prospects and Mineral Resource Statements. Presentation to the Professional Geoscientists Ontario. [ Links ]

Rupprecht, S. 2004. Establishing the feasibility of your proposed mining venture. Proceedings of the International Platinum Conference 'Platinum Adding Value. The South African Institute of Mining and Metallurgy, pp. 243-247. Securities and Exchange Commission. 2018. Final Rule: Modernization of Property Disclosures for Mining Registrants (sec.gov). https://www.sec.gov/rules/final/2018/33-10570.pdf [accessed 07 December 2022]. [ Links ]

Rupprecht, S.M. 2020. Future trends in the international Reporting Codes based on SEC's Regulations SK-1300. Journal of the Southern African Institute of Mining and Metallurgy, vol. 120, no. 12, pp. 659-664. [ Links ]

SEC. 2018. Modernization of Property Disclosure for Mining Registrants. https://www.sec.gov/corpfin/secg-modernization-property-disclosures-mining-registrants [ Links ]

Steele-Schober, T. 2021. The Importance of ESG for Mineral Reporting. Journal of the Southern African Institute of Mining and Metallurgy, vol. 121, no. 6, pp. 8-11. [ Links ]

The South African Environmental, Social and Governance Committee (SAMESG) Committee. 2017. The South African guideline for the reporting of environmental, social and governance parameters within the solid minerals and oil and gas industries. Version 2.0. [ Links ]

Correspondence:

Correspondence:

S.M. Rupprecht

Email: rupprecht.steven@gmail.com

Received: 26 May 2023

Revised: 29 Jan. 2025

Accepted: 13 May 2025

Published: June 2025

1 The SK-1300 proposing release explained that an "initial assessment is not a scoping or conceptual study as defined in some of the CRIRSCO-based codes or a preliminary economic assessment as defined in Canada's NI 43-101.621. The purpose of an initial evaluation is narrower than those studies as it would be done solely to support the disclosure of mineral resources and not to determine whether to proceed with further work to prepare a prefeasibility study for mineral reserve determination.''