Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

On-line version ISSN 2222-3436

Print version ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.24 n.1 Pretoria 2021

http://dx.doi.org/10.4102/sajems.v24i1.3784

ORIGINAL RESEARCH

Not all experts are equal in the eyes of the International Auditing and Assurance Standards Board: On the application of ISA510 and ISA620 by South African registered auditors

Marianne Kok; Warren Maroun

School of Accountancy, Faculty Commerce, Law and Management, University of the Witwatersrand, Johannesburg, South Africa

ABSTRACT

BACKGROUND: The article focuses on inconsistencies in audit approaches when auditors place reliance on the work performed by others. It examines differences in the approach followed by auditors when relying on the work of a predecessor versus the work of an auditor's expert.

SETTING: The study contributes to the limited body of auditing research focusing on the technical application of International Auditing Standards and the functioning of actual audit practice in a South African context. It outlines how auditors apply their professional judgement when using technical auditing standards when comparing the work of a similarly trained expert in the field of accounting and auditing (per ISA510) versus the work of an expert in a field other than accounting and auditing (per ISA620).

AIM: The purpose of this article is to examine and identify inconsistencies in the interpretation and application of ISA510 and ISA620 by a purposefully selected number of registered auditors in South Africa. It considers how inconsistencies in the approach followed when an auditor places reliance on the work of another auditor or an auditor's expert points to underlying efforts to seek legitimacy and manage legal liability.

METHOD: Detailed interviews are used to explore auditors' experiences and challenges with the application of these two ISAs.

RESULTS: Audit quality is not necessarily a function of compliance with professional standards. While ISA510 and ISA620 deal with a situation where an auditor places reliance on the work of a third party, they are interpreted and applied very differently.

CONCLUSION: The application of ISA510 is part of a rules-based approach to auditing aimed at reducing an auditor's legal liability rather than enhancing audit quality. The same logic applies to ISA620 except that auditors perceive that their risk exposure is lower because the standard is limited to a single transaction or balance rather than to the entire audit engagement. The application of ISA620 is also useful for convincing internal reviewers, external regulators or audit committees that sufficient appropriate evidence for a complex line item has been obtained. The need to ensure a more robust process for testing complex balances and transactions is not, however, the primary consideration. Regulators and standard setters should not assume that compliance with auditing standards results in better quality audits. At the operational level, the need to manage legal liability and to signal the credibility of test procedures may be more relevant for the execution of audits than ensuring that audit opinions are supported by sufficient appropriate audit evidence. As only two standards, applied in a single jurisdiction, are used to illustrate this point, additional research will be required to determine the extent of inconsistency in the application of auditing standards and how this can result in lower levels of audit quality.

Keywords: auditor's expert; audit quality; International Auditing and Assurance Standards Board; IAASB; predecessor auditor.

Introduction

Users, auditors, regulators and general society have different views on audit quality. Users think that high audit quality means the absence of any misstatements in financial information. Regulators tend to view high audit quality as compliance with professional standards (Christensen et al. 2016; DeFond & Zhang 2014; Knechel et al. 2012). The auditor may define high audit quality according to their internally developed audit approaches or methodologies. These evolve as society's information needs change, amendments to regulatory requirements are introduced and clients' value creation processes mature (Peecher, Schwartz & Solomon 2007). Key for defining and evaluating audit quality are the provisions of the applicable auditing standards.

Considerable time and effort are invested in the development and improvement of technical guidelines (Burns & Fogarty 2010; Byington & Sutton 1991; Humphrey, Loft & Woods 2009). While these have not been able to prevent every corporate failure, the codification of acceptable audit practice has been important for ensuring consistent execution of audit engagements, monitoring and review of audit practice and minimum levels of audit quality (see also Humphrey et al. 2011; Maroun & Solomon 2014; Power 2003a). An example is the framework on audit quality issued by the International Auditing and Assurance Standards Board (IAASB).

The objectives of the framework are to raise awareness about the key elements of audit quality, encourage ways to improve audit quality and facilitate dialogue among key stakeholders (IAASB 2014). The framework is complemented by International Standards on Quality Control (ISQC1) - which deals with the development and maintenance of quality designed to provide a governance schematic for audit firms - and Quality Control for Audit of Financial Statements (ISA220), which guides quality control at the engagement level (Bedard et al. 2008). Collectively, these standards are designed to address each 'element' of the audit quality paradigm.

Exactly how standards impact audit practice has not been considered in detail. We know very little about how audit firms interpret and apply professional standards to ensure high-quality audit engagements. The majority of international research focuses on inputs or variables that may affect audit quality such as the size of the audit firm (DeAngelo 1981; Lawrence, Minutti-Meza & Zhang 2011), length of audit tenure (Geiger & Raghunandan 2002; Jackson, Moldrich & Roebuck 2008), legislation (Kleinman, Lin & Palmon 2014) and different skills of engagement leaders (Martinov-Bennie & Pflugrath 2009; Nelson 2009; Simnett, Carson & Vanstraelen 2016). The outputs of the audit process have also been tested extensively. For example, there is a large body of work that deals with the effect of external audit on earnings quality (Becker et al. 1998; Piot & Janin 2007), the accuracy of going concern reports (Carson et al. 2012; Geiger & Rama 2006) and recommendations for changes in the content and structure of different audit reports (Mock et al. 2012; Turner et al. 2010). Technical analysis of audit processes appears to have been overlooked (Maroun & Jonker 2014).

With the above points in mind, the objectives of the current article are twofold. The first is to present the interpretation and application of ISA510 and ISA620 by registered auditors (RAs). The second is to explore inconsistencies in approaches followed when applying the two standards.

The study focuses specifically on ISA510 and ISA620 because of curious differences in the approach that is followed when an auditor places reliance on the work of another auditor or an auditor's expert.

In substance, the standards deal with a similar situation: an auditor is placing reliance on the work of a third party to collect sufficient appropriate audit evidence. Nevertheless, as discussed below, it appears that relying on the work of an auditor's expert is less onerous than placing reliance on the work of another auditor.

This is despite the fact that a fellow auditor would be subject to the same technical training, professional development and regulatory oversight as the incumbent. In this context, differences in the two standards, coupled with variations in how they are interpreted and applied in practice, can reveal factors (other than the technical requirements in auditing standards) that affect the audit process.

The researchers acknowledge that other standards, notably ISA610, also involve an auditor placing reliance on the work of others. These standards are not specially considered in this article because, at the time of writing, the use of ISA510 and ISA620 was more common following the South African regulator's decision to introduce mandatory firm rotation (effective in South Africa from 2023). As with any research of this type, delimitations are also required to retain focus. A more detailed review of inconsistencies in the ISAs and differences between the ISAs and other assurance standards is deferred for future research.

Despite the above delimitation, the article makes an important contribution. It provides empirical evidence on how auditing standards are being interpreted and applied by RAs in a real-world setting, adding to the limited body of interpretive research on auditing (Power 2003b) especially from a South African perspective (Maroun & Jonker 2014). The research also identifies key considerations for the application of two commonly used auditing standards (including key risk areas), challenges encountered and technical inconsistencies. These findings will be useful for auditors seeking to improve audit quality and for standard setters who need to ensure internal consistency of audit practice.

The remainder of this article is organised as follows: a review of the applicable academic and professional literature, and a summary of the method followed and the rationale for using an exploratory research design. Then the findings are discussed followed by the conclusion and ideas for further research.

Literature review

To obtain reasonable assurance, the auditor must gain an understanding of the client, its business environment and relevant internal controls (Bentley, Omer & Sharp 2013; IAASB 2013, 2019). This will entail performing risk assessment procedures in the audit planning phase to assess the risks of material misstatement at the overall and assertion level (IAASB 2019), following which the auditor designs suitable test procedures to reduce audit risk to an acceptably low level (Hogan & Wilkins 2008; IAASB 2009f). Audit risk is the risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated. As audit risk is a function of the risk of material misstatement and detection risk (IAASB 2009b:para 5) it is important to gather sufficient appropriate audit evidence to ultimately support the auditor's opinion (IAASB 2009g). Of interest for this research is the application of ISA510 and ISA620 as part of the process of reducing audit risk.

ISA510 - Initial audit engagements

ISA510 deals with three areas: opening balances, consistency of accounting policies and relevant information in the predecessor auditor's report (IAASB 2009h:para 5,7-9). The standard should be read with ISA300 which refers to quality control for an audit of financial statements and communicating with the predecessor auditor when there has been a change of auditors (IAASB 2009e:para 13).

Procedures for evaluating opening balances include: (1) the review of the predecessor auditor's workpapers to obtain evidence regarding the opening balances, (2) evaluating whether or not audit procedures performed in the current period provide evidence relevant to opening balances or (3) performing specific audit procedures to obtain evidence regarding opening balances (IAASB 2009h:para 6(c)(i)-(iii)). The review of the predecessor auditor's workpapers is influenced by the professional competence and independence of the predecessor auditor (IAASB 2009h:para 4; IFAC 2008). The requirement to consider the independence and competence of the predecessor auditor appears similar to the guidance provided in ISA600. However, the IAASB asserts that an incoming auditor is not to place reliance on the work of a predecessor auditor while, in ISA600, an auditor may place reliance on the work of a component auditor (International Federation of Accountants [IFAC] 2008).

In evaluating the work of the predecessor auditor, the auditor applies professional judgement and professional scepticism. The former stems from the application of rigorous formal training, knowledge and experience (Jones, Massey & Thorne 2003; Nelson 2009). Both the incoming and predecessor auditor's ethical standards affect the application of professional judgement. Finally, if the incoming auditor could not obtain sufficient appropriate audit evidence regarding opening balances, the auditor will modify the audit opinion (IAASB 2009h:para 10).

ISA620 - Using the work of an auditor's expert

If an auditor has limited expert knowledge to obtain sufficient appropriate audit evidence, the assistance of an auditor's expert will be considered. The application of ISA620 is summarised as follows: firstly, the auditor is required to assess whether expertise in fields other than accounting or auditing is required. If so, the auditor will determine whether or not to use the work of an auditor's expert (IAASB 2009i:para 7). Secondly, when an auditor's expert is used, the nature, timing and extent of audit procedures should consider factors such as the nature of the matter to which that expert's work relates, the associated risks of material misstatement and the significance of that expert's work (IAASB 2009i:para 8(a)-(e)). Thirdly, the auditor will evaluate if the auditor's expert has the necessary competence, capabilities and objectivity for the auditor's purposes. In the case of an auditor's external expert, an evaluation of objectivity will include inquiry regarding interests and relationships that may create a threat to that expert's objectivity (IAASB 2009i:para 9).

Fourthly, the auditor will obtain a sufficient understanding of the field of expertise of the auditor's expert to enable the auditor to determine the nature, scope and objectives of that expert's work and evaluate the adequacy of work performed (IAASB 2009i:para 10(a)-(b)). Finally, the auditor will agree in writing on relevant matters with the auditor's expert. These include, for example, the nature, scope and objectives of that expert's work (IAASB 2009i:para 11(a)-(d)).

The auditor must evaluate the adequacy of the auditor's expert's work (IAASB 2009i:para 13, A38-A39).

If the auditor determines that the work of the auditor's expert is inadequate for the auditor's purposes, the auditor will agree with that expert on the nature and extent of further work to be performed by that expert or perform additional audit procedures (IAASB 2009i:para 13). The auditor will not usually refer to the work of an auditor's expert in an auditor's report containing an unmodified opinion unless required by law or regulation to do so (IAASB 2009i:para 15, A42).

Comparison of ISA510 and ISA620

Table 1 shows a comparison of ISA510 and ISA620 in terms of audit activity and process.

The difference in the application of audit standards

From an agency theory perspective, external audits play a key role in addressing information asymmetry (Watts & Zimmerman 1983). It follows that, as the risk that financial statements are misstated increases, the auditor must perform more rigorous and extensive testing to avoid issuing an incorrect audit opinion (IAASB 2009a) and ensure that agency-related costs are mitigated (Watts & Zimmerman 1983). For example, an increase in risks of material misstatement might be addressed by relying on more substantive tests, in addition to tests of controls, which are designed to collect audit evidence over extended periods based on larger sample sizes (IAASB 2009f, 2009g, 2013). Similarly, the decision to engage an expert to test complex balances and transactions and the work performed by the auditor to corroborate the expert's findings should be informed by the assessed level of audit risk (IAASB 2009h, 2013, 2018). The same logic should apply when it comes to the nature and extent of the work performed by an incoming auditor to support conclusions on opening balances tested by the predecessor auditor (IAASB 2009h). As a result, variations in the process followed by an auditor before deciding to rely on the work of either an expert or another auditor should reflect the differences in the risks of material misstatements going undetected.

An audit of financial statements is not only a technical function designed to reduce agency costs. As explained by Power (1991, 1994, 1995) and Humphrey and Moizer (1990), an audit can only confer legitimacy on financial reporting if the audit itself is accepted as legitimate. As a result, the 'rituals of verification' may be more important than the technical operation of the audit process itself (Power 2003b; Unerman & O'Dwyer 2004). This is especially true when considering that the users of the audit report are unable to observe exactly how an audit has been executed. They must rely on the good-faith assumption that, because an audit was conducted by an independent expert exercising due care and skill, that audit results in more reliable financial reporting (Power 2003b; Unerman & O'Dwyer 2004). Consequently, the application of auditing standards may have more to do with demonstrable displays of compliance with the respective standards to reassure the user of an audit report than with the substantive reduction of audit risk (Power 2003b; Unerman & O'Dwyer 2004). Managing legal liability is a key part of this ceremonial process. Legal disputes with clients and third parties can result in direct and material financial losses for an auditor.

Claims of negligence or professional misconduct are also a powerful signal of poor audit quality (Palmrose 1988, 1997). They can have adverse implications for professional reputation and the confidence that users of an audit report and non-experts vest in the practitioner. As a result, the implementation of auditing standards, including those dealing with the use of experts and the work of other auditors, will be influenced by the need to mitigate legal liability in addition to reducing audit risk for technical purposes (Botez 2008).

Before exploring this possibility in more detail the following section outlines the approach followed to collect and analyse data.

Method

As explained by O'Dwyer et al. (2011:38), a qualitative approach is most appropriate when examining seldom studied issues.1 Qualitative research designs are well suited to exploring processes, techniques and practices where relationships cannot be defined and measured in a positivist sense. An interpretive approach to collecting and analysing data allows the researchers to highlight how the technical requirements of ISA510 and ISA620 are understood and operationalised in different practical contexts and reveal any inconsistencies in their application (see Brennan & Solomon 2008; Maroun 2012; O'Dwyer et al. 2011; Thomas 2006). The intention is not to generalise or extrapolate results but to explore auditors' views on two important but seldom studied professional standards and how these standards influence audit practice in a real-world setting (see Brennan & Solomon 2008; O'Dwyer et al 2011; Rowley 2012).

Data collection

Purposeful sampling was used to select respondents. All respondents are RAs. Their experience and the sectors that they audit are summarised in Appendix 1. The sample consisted of audit partners from the Big 4 (8 respondents), second-tier firms (6 respondents) and small firms (6 respondents).2 The aim was to ensure that findings were not influenced by the type of audit firm or industry specialisation. It should, however, be noted that the intention is not to consider if specific industry experience, type of audit firm or other variables (such as cultural background) are associated with different views on the technical provisions of ISAs. The number of interviews was informed by the point at which 'saturation' was reached. This occurred after 14 interviews were completed (adapted from Leedy & Ormrod 2015).

All interviews were semi-structured to ensure a thorough examination of the subject matter while retaining focus on the research question (Holland & Campbell 2005; Leedy & Ormrod 2015; O'Dwyer, Owen & Unerman 2011; Rowley 2012). Interviews were conducted in Johannesburg and Pretoria from November 2014 and March 2015 and lasted between 40 and 70 min.

Questions dealing with the technical provisions and execution of the requirements in ISA510 and ISA620 were included in the interview agenda followed by open-ended questions dealing with the interviewees' views on the similarities and differences of these two standards (Rowley 2012; Ryan, Scapens & Theobald 2002). The interview agenda was reviewed by two researchers at the authors' host institution. It was also piloted with a RA at one of the Big 4 to ensure that it covered the relevant provisions of ISA510 and ISA620, is accurate and focuses on the research questions. The pilot interview resulted in no significant adjustments to the interview questions.

Interviewees were provided with an overview of the nature and purpose of the research and invited to participate in the study. Interviews were conducted in person with the exception of one telephonic interview (R5).

Data analysis

The researchers focused on how the requirements of ISAs were explained by the respondents and how these provisions were being applied. No detailed coding was done at this stage as the aim was to gain a general sense of how respondents were operationalising the professional standards. The second step focused on the development of categories or emerging themes in the data (open codes). Examples included reasons for changing auditors, technical disagreements among auditors, different views on the technical requirements of the standards and procedures performed when accepting new clients or using the work of experts (adapted from Leedy & Ormrod 2015; Rowley 2012).

The open coding process required each transcript to be read several times. The coding was also an iterative exercise with transcripts being recoded as additional interviews were conducted. No new open codes were noted after the 14th interview. After all of the transcripts were coded, the open codes were aggregated under axial codes. These were guided primarily by ISQC1 and ISA220 and included: competency of the auditor or auditor's expert, the importance of independence, staffing considerations and difference in audit strategy or approach.

Any quotations that may result in the identification of respondents have been paraphrased or amended with changes indicated. Participants were interviewed at their choice of location. Interviewees could also discontinue the interview at any time. Finally, as interviews can be classified as moral enquiry, the required ethics clearance was obtained from the authors' university.

Results

Interviewees' understanding of the application of ISA510 and ISA620 are presented below. Differences in the use and interpretation of the two standards are outlined thereafter.

ISA510

Respondents discussed several instances where ISA510 is relevant. Each is discussed below.

Risk assessment - Review of financial statements

The risk assessment for listed entities differs from privately owned entities as the needs of the stakeholders are different (R1, R3, R8, R9). For example, consideration is given to what management may attempt to overstate or understate and potential fraud areas (R1). A common departure point for performing the risk assessment is a review of the most recent financial statements to determine the materiality and potential future impact of each financial statement line item (R1, R2, R3, R4). Basic analytical review of the previous year's financial statements is used to 'understand the numbers', the 'history of movement in account balances' and 'types of audit reports issued' (R13). In addition, the status of the previous audit report and the presence of any possible reportable irregularity are considered (R11, R20).

Compliance with the International Financial Reporting Standards

The review of financial statements involves evaluating whether there are complex balances and transactions. The aim is to assess the risk of a disagreement between the incoming auditor and the client because of differences in the interpretation of accounting standards. One expert explained as follows:

'The last thing you want to identify is the previous auditor had a disagreement on a technical matter that the client is shopping around to get the right opinion and that you then accept the client and challenged with a similar view.' (R2, former auditor and audit committee chair, financial services)

Review of the financial statements provides a sense of whether the accounting framework and selected accounting policies have been complied with or not (R16, R17). R1 and R2 commented explicitly on the difference in interpretation of the application of IAS39 and IFRS9 among the Big 4 relating to areas of judgement. Areas of possible restatement due to a difference in interpretation of the International Financial Reporting Standards (IFRS) need to be raised early in the new client-auditor relationship (R1, R2, R3, R4).

Review of predecessor auditor's workpapers

Compliance with selected accounting policies is validated when reviewing the predecessor auditor's workpapers. Analytical review of financial performance is key, with special attention given to areas where management judgement is present and how these areas have been disclosed in the financial statements (R2, R4, R5). Attention is given to previous year's issues reported by the external auditor to management and the schedule of unadjusted audit differences (R5). The accounting framework adopted and the application of certain IFRSs are considered, specifically where there may be a difference in interpretation among the audit firms. Where the opening balances have not been subjected to an audit in the prior year, the opening balances will be subjected to a full audit to ensure that they do not have a material impact on the current year's results (R4).

Access to the predecessor auditor's workpapers is a key consideration. This is usually 'dependent on who the predecessor audit partner was and not so much the firm' (R5). All of the respondents felt that, where access to workpapers was restricted, this was a potential indicator of deficient audit practice or a breakdown in the relationship between the predecessor auditor and client. In both instances, the assessed risks of misstatement are seen as higher and more rigorous testing of the opening balances will be required. Finally, more reliance or comfort is gained when the predecessor auditor is a firm with international alliances (R5). This may be because of the international brand as a type of collateral for the quality of the outgoing auditor's work (R4; R19).

Nature, timing and extent of procedures by the incoming auditor: In some instances, a verbal discussion with the predecessor auditor is sufficient to conclude on opening balances if the initial risk assessment is low. The Big 4 seldom obtain clients from smaller audit firms while there is some client movement between the Big 4 and the second-tier firms (R1, R2, R3).

For a listed entity, the initial review will be performed by a partner and, for smaller entities, by a competent manager with monitoring and review by the partner (R1, R2, R3 and R4). For other firms, a senior manager with some partner supervision will take place (R5, R6, R9 and R10).

As touched on earlier, examining the predecessor auditor's workpapers is the preferred approach for evaluating opening balances. The main objective is to understand the predecessor auditor's assessment of materiality and errors found. If available, the schedule of adjusted and unadjusted audit differences will be reviewed or discussed with the predecessor auditor (R1, R2, R3, R4). The schedule of unadjusted differences assists with 'the identification of a possible trend for misstatements' (R4). Management letters about audit findings from the prior year, if made available, will also be scrutinised to establish the risks of misstatement in opening balances. If possible, a review of the main assertions will be helpful to understand the scope of the prior year's work (R3).

The discussion or meeting with the predecessor partner provides further information about the opening balances. The aim is to identify areas of concern noted by the previous auditor and gain a sense of skill and competency of the previous audit team. This can consider, not only the work done at the current client, but also the outgoing partners' portfolio and how long the partner has been in practice:

'You ask: "What other clients are you doing?" "How long have you been the auditor of this one" and "How long have you been an auditor?" Those basic things - to understand independence and to understand competency - are an integral part of the nature, timing and extent of the procedures carried out under ISA510.' (R3, audit partner, consumer goods and services)

If access to the workpapers of a predecessor auditor is restricted, alternate procedures on opening balances are performed. Examples include walkthrough procedures or tests of detail (R14). The application of accounting policies is also reviewed. For example, the approach for determining if debtor balances are impaired and the application of IFRS9's expected loss model are evaluated (R1).

Planned rotation of audit partners (within the same firm) is different from a change in audit firm. In most cases, the incoming auditor will shadow the exiting auditor (R2, R3). A 'roll-forward of balances and a conversation will take place' between the outgoing and incoming audit partners (R3, R4, R5). The competence of the previous engagement leader will still be considered (R3, R4). For the Big 4 firms and the second-tier firms, the prior year's audit files would have been subjected to internal quality reviews providing a basis for assessing the rigour of procedures performed on the prior period's balances and transactions (R3). The audit team and, in most instances, the audit manager are still allocated to the audit client (R1, R2, R3, R4, R5).

The rationale for ISA510: Respondents had different views on the inclusion of specific procedures in ISA510. The most commonly held view was that these procedures are part of the Big 4 and second-tier firms' risk management processes which, over time, have become a generally accepted basis for testing opening balances and have, therefore, been codified (R1; R15; R17).

The standard stipulates minimum procedures but, based on the risk associated with the audit client, 'the depth of the audit work will vary' (R4, R5). A slightly different interpretation of ISA510 is that its prescribed procedures are not necessarily about enhancing audit quality directly but rather about lowering the auditor's risk of legal liability. As a result, there was a sense that ISA510 developed in response to specific facts or circumstances encountered in practice. Performing a specific set of procedures becomes a taken-for-granted part of the audit firm's policies for managing its business risks (R1; R12).

Respondents agreed that there were no laws or regulations that directly mandated the application of the procedures in ISA510. Nevertheless, they felt that they were expected to comply with all the procedures. For example, irrespective of differences in facts or circumstances, all respondents indicated that they will review any available financial information to determine what was included in the prior period's financial statements. This includes a review of management's accounting policy choices. Concerns that the audit firm may have with the auditee's industry are also taken into consideration (R2). Similarly, while auditors may be able to justify excluding clearly immaterial balances from the scope of ISA510 testing:

'[T]here are certain minimums … [ISA510] is one of the standards that you can't bypass so you can't say, "Well, there is no risk in opening balances: I am doing nothing".' (R4, audit partner, consumer goods and services)

Respondents justified the strict adherence to ISA510 on the grounds that access to the previous auditor's workpapers may not be available. In these cases, ISA510 provides a practical solution for concluding on opening balances. Similarly, the procedures prescribed by ISA510 are useful if the previous auditor has not divulged all the relevant information relating to the opening balances. In this instance, ISA510 is useful for providing a basis for reaching a conclusion on opening balances and demonstrating that the incoming auditor has obtained sufficient appropriate evidence over the opening balances (R5). In addition:

'If the opening balances are wrong you are going to get a wrong end result. It also provides you with an opportunity to gain knowledge of the client's business and it enables you to get some indication of how the client operates especially with small businesses.' (R8, audit partner, financial servies)

There was also a view that having too much discretion to determine the nature, timing and extent of procedures for opening balances would lower audit quality. This is predicated on the view that, given the increased focus on external regulation of the profession, specific audit procedures should also become more prescriptive:

'The auditing profession is fairly regulated and risk-focused. Auditors have an accustomed mind set to pre-engagement activities as part of planning. I think the problem with standards is that they become too vague so that you allow for too much judgement which means that there is potentially too much room for error.' (R3, audit partner, consumer goods and services [author's own emphasis])

Importantly, the quality of the audit evidence provided by prescriptive procedures was not discussed. In addition, respondents could not give examples of exactly how the use of prescriptive procedures improved audit quality. It is sufficient for practitioners to conclude that the nature, timing and extent of their approach for testing opening balances is sufficient because it covers each of the recommended procedures in ISA510 (R1, R4).

Other ISA standards contain a fair amount of professional judgement in the sense that:

'… you assess a risk and respond to it.' (R4, audit partner, financial services).

The auditor's response to the level of risk is based on knowledge, experience and competencies. When dealing with opening balances, the incoming auditor is not privy to information relating to the prior period. As a result, respondents feel that ISA510 'forces the auditor by mandating procedures to ensure that the incoming auditor is covering something' (R4, audit partner, financial services).

Respondents felt that the detailed procedures listed in ISA510:

'… make logical sense without considering access to the predecessor auditor.' (R4, audit partner, financial services).

This finding can probably be attributed to the appearance of a quasi-scientific approach to testing opening balances which, on the surface, appears to be objective and rigorous (see Humphrey et al. 2011). ISA510 defines specific procedures that need to be performed to demonstrate that sufficient appropriate evidence has been collected. There is little judgement being applied when determining which of these procedures need to be applied and the extent to which they are being relied on. The procedures are also applied without having to place significant reliance on judgements by the predecessor auditor. As a result, respondents suggest that ISA510 is a useful risk management tool because it creates a clear distinction between audit work performed by the predecessor and incoming auditor. Because the incoming auditor has 'objectively' tested opening balances, any errors or omissions of the predecessor auditor are, in essence, 'quarantined' (R3, R4).

Ironically, while the user of the audit report can rely on the opinion of the predecessor auditor, the same is not the case for one auditor seeking to rely on the work of another auditor (R10). In other words, non-expert users can place reliance on claims to professional expertise and independence of the predecessor auditor but, within the profession, professional appearance alone is not enough. This is because the credibility of work performed is being defined based on adherence to formalised test procedures in ISA510 and not the good-faith assumption that all auditors are equally competent (R10):

'Auditors are just human beings, an honest mistake can be made or a deliberate mistake can be made. Not all auditors are professional.' (R9, associate director, mining and industrials)

In this context, normative pressures to perform procedures required by ISA510 have encouraged the development of internal or firm-level policies that take a procedural approach to testing opening balances. For individual members of the firm, the result is a drive to comply with internal policy and, by default, ISA510.

For example, respondents explained that electronic workpapers are utilised by the Big 4. Their audit software is designed to generate predetermined procedures based on the ISAs and other regulatory requirements (R1, R2, R3, R4). These procedures can be mandatory and the individual auditor cannot proceed to the next workpaper or online screen unless the procedure has been considered. Alternately, approval from senior partners or representatives from technical departments is required if an auditor attempts to ignore one of the ISA510 procedures. This is designed to ensure that, at minimum, risk areas and materiality relative to the current year financial statements have been addressed and that the firm can claim compliance with the ISAs (R1, R2, R3, R4).

ISA620 - Auditor's expert

Respondents outlined two broad instances when ISA620 is applicable: when the audit team does not have sufficient skills to test a balance or transaction and when the use of an expert provides complementary audit evidence.

As clients' business models become more complex, multidisciplinary skills become essential for understanding audit risks and designing audit procedures to obtain sufficient appropriate audit evidence (R1, R2, R5). ISA620 is applicable when required skills are clearly outside the scope of the professional accountant's expertise (R12).

There were also instances where experts were being used to complement the audit team's skills. These typically involved the use of actuaries or qualified valuators to assist with complex mathematical models needed for valuing assets and liabilities such as defined benefit obligations, pension plan assets, credit loss models under IFRS9 and sensitivity analyses under IFRS7 (R2, R3).

In most instances, these experts were engaged when the applicable accounting standards required the use of a fair value measurement or disclosure. Respondents confirmed that most cost-based accounting standards (such as IAS2, IAS16 and IAS38) seldom require the use of an expert. In contrast, accountants and auditors appeared to be less comfortable with the methods used to determine fair values in terms of IFRS13 and the assumptions of different valuation models. In these cases, an expert is used to provide the necessary assistance, even though, on strict reading of ISA620, the auditor should be in a position to test these fair values without having to rely on an expert (R8, R9, R10).

Audit clients frequently rely on experts to assist with the measurement of different assets and liabilities.

Respondents pointed out that, when a client makes use of a management expert, the auditor will typically use his or her expert to verify the work performed by the management expert (R1, R3, R7). This was justified because the use of an auditor's expert is the most efficient and appropriate approach for confirming complex judgements and estimates made by the audit client's expert (R1, R2, R5).

As a result, a primary objective of ISA620 is to distinguish between the sufficiency and appropriateness of evidence provided by a client's and an auditor's expert. While these experts may be similar in most respects, the former may lack the same level of independence and objectivity of the audit expert due to a close working relationship with the client (R1, R3, R4, R6). As a result, an auditor cannot rely exclusively on the work of a management expert (see also ISA500). Additional audit procedures are required to confirm that key assumptions, chosen methods and the scope of any work performed are sufficient to address the relevant audit risk and to support a conclusion on the respective balance or transaction (R1, R3, R4, R7).

Even in cases when a management expert is not used, some respondents felt that an audit expert could be used to complement procedures performed by the audit team on different balances or transactions, especially when these have the potential to become material in future periods (R4). For these respondents, ISA620 provided a framework for using a form of third-party verification usually to provide confirmatory evidence of the results of the auditor's test procedures.

Nature, timing and extent of procedures

The nature, timing and extent of audit procedures consist of an assessment of an auditor's expert's competence, communication of scope of work, agreeing to the format of deliverables and testing the auditor's expert's findings (IAASB 2009i:para 9, 11-12).

The assessment of competence, where the auditor's expert is not employed by an audit firm, is based on the person's qualification and experience (R3). Scope of work to be performed, due date and the format of the deliverable are agreed in writing with the auditor's expert (R1, R2, R3, R4). Where an auditor's expert is already in the employment of an audit firm, the scope of work is also communicated with the auditor's expert.

However, the format of the deliverable is known to the auditor's expert who would have been informed of the firm's audit methodology (R1, R2, R3, R4). In this case, the auditor's expert is seen as another member of the audit team and is familiar with the audit firm's quality control policies and procedures (R3, R4).

Once the deliverable is received from the audit expert, detailed testing of the report or findings takes place.

This involves the testing of assumptions or estimates applied. Assumptions or estimates are tested or verified, usually by the audit supervisor or manager. Any input data (for example, interest rates or statistical data) are verified against available market data. If a certain methodology was used, this will be tested against other available models and approaches as a reasonability check (R3, R6).

Rationale for ISA620

The two primary reasons for the application of ISA620 were the lack of skills by the engagement team to test certain balances and transactions or the need to obtain complementary audit evidence. In addition to these technical justifications for using ISA620, respondents suggested that the standard can be used (in some cases) to limit the auditor's legal liability. Respondents feel that the audit evidence provided by ISA620 may be more persuasive than the result of test procedures completed by an audit team. This is because the work has been prepared by an individual with specialised skills or experience and was less likely to be questioned by a third party. Consequently, using an auditor's expert was a useful approach for testing a balance or transaction associated with a high level of legal liability risk (R1, R7, R8).

There were, however, instances of auditors applying ISA620 by default. Instead of considering the nature of the respective balances and transactions, including inherent risk, some respondents automatically concluded that an expert would be required to provide sufficient appropriate audit evidence for material balances (R6, R7, R10). One respondent provided an example concerning a non-monetary asset that was valued by an expert in prior years. Even though the state of the asset and the applicable market had not changed, the asset was re-assessed each year by an independent expert (R7). Similarly, even in instances where fair value measures were being computed under IFRS13, experts were engaged to support the work of the audit team because this had become standard firm procedure (R10).

As the use of an expert becomes more common on audit engagements, the application of ISA620 becomes a basis for demonstrating that sufficiently rigorous procedures have been applied to support an opinion on complex balances and transactions. In other words, the standard is not being used as part of a rational response to assessed risks of misstatement but as part of a symbolic demonstration that the approach followed for the current audit engagement is consistent with that used in prior periods or by other professional firms (R7, R10).

Under ISA620, the individual engaged to assist the auditor must be a recognised subject expert. The standard also refers to the importance of formal training and membership of recognised professional bodies (IAASB 2009i:para A9, A15). This is complemented by an assessment of the appropriateness of the methods applied by the expert, any assumptions used and the scope of the work performed (IAASB 2009i:para A33). Similarly, the confidence that non-expert users place in the audit opinion is based on the codification of audit methodology, the appearance of rational technical audit procedures and the competency of the independent practitioner. In this way, ISA620 does more than articulate technical processes that are followed when an auditor engages an expert to assist with testing balances and transactions. It provides the discourse for articulating the features of expertise that the layman values in the auditor and that, by analogy, the auditor identifies in the duly appointed expert.

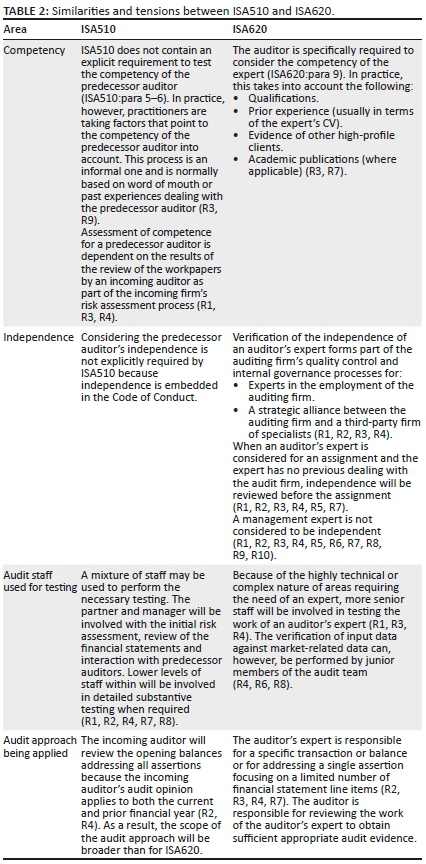

Similarities and tensions between ISA510 and ISA620

Table 2 summarises the differences in the application of ISA510 and ISA620 discussed by the interviewees.

Discussion, conclusion and areas for future research

All of the respondents agreed that ISA510 and ISA620 provide important guidance on assessing the risks of misstatement applicable to the respective balances and transactions and inform the approach that needs to be followed to reduce that risk to an acceptably low level. As a result, the application of these standards almost always requires the involvement of the audit manager and partner. The importance of professional judgement and scepticism when applying both standards also makes them a focal point for a quality review partner or internal peer review under ISQC1.

Differences in the way in which ISA510 and ISA620 are applied reflect the fact that the standards deal with different circumstances. Most notably, the former is applicable for evaluating all the opening balances (and accumulated prior transactions) while the latter is usually limited to testing a select number of financial statement line items. Variations in how the requirements of the two standards are operationalised also reflect auditors' personal beliefs about the rationale for the standards rather than the express objectives for each standard as outlined by the IAASB.

ISA510 is intended to provide a framework for ensuring that opening balances are tested in sufficient detail to ensure that the incoming auditor provides an appropriate opinion on a new client's financial statements (IFAC 2008). In practice, the standard is seen primarily as a means for reducing the auditor's risk of legal liability. Auditors acknowledge that, while ISA510 does not mandate the execution of every specified procedure, practically, all the standard's listed procedures are applied irrespective of whether or not this is beneficial for the integrity of the audit. The reason: by executing audit procedure on a client's opening balances, the work of the predecessor auditor, including any omissions or errors, can be separated from testing carried out by the incoming practitioner. With risk management - rather than the technical rigour of the audit engagement - being the primary consideration, ISA510 is applied legalistically rather than as part of the normal risk-based audit model.

ISA620 is applicable where the auditor requires specialised knowledge or expertise. At the technical level, respondents agree that, as a client's business models become more complex, multidisciplinary skills become essential for understanding audit risks and designing audit procedures to obtain sufficient appropriate audit evidence. The use of an expert is also desirable when the transaction or financial statement line item is associated with a high level of legal liability. More relevant than limiting legal exposure is the value of ISA620 for legitimising the test of a material balance or transaction.

The layman places reliance on the auditor's opinion on a client's financial statement without a detailed understanding of exactly how the financial statements have been tested. As explained by Power (2003a, 2003b), the rituals of verification matter more than the mechanics of the audit process itself for the audit opinion to be accepted as legitimate. The same applies at the level of the auditor testing a specific balance or transaction. Using the work of an expert is an efficient and easy-to-apply technique for convincing internal reviewers, external regulators or audit committees that sufficient appropriate evidence for a complex line item has been obtained. An expert can also be used to bolster the auditor's confidence and lower any risks to personal reputation by providing corroborating conclusions on different 'elements' of the financial statements.

These findings have several important implications. Firstly, they explain variations in the application of technical auditing standards. When the aim is to create a type of firewall and limit legal liability, standards are applied legalistically. The number of audit procedures performed is increased and the scope of the testing is broad in the sense that multiple balances and transactions must be addressed. When the objective is to corroborate findings and legitimise audit work, additional testing can be focused on the specific balance or transactions. Legitimacy is not secured by performing additional procedures, expanding sample sizes or focusing on multiple financial statement line items but by engaging an expert to test the most complex balance or transaction.

Secondly, audit quality is not necessarily a function of compliance with professional standards. If guidance in particular standards is applied only for symbolic purposes or for limiting legal liability, the fact that audit procedures outlined by the IAASB have been executed does not guarantee a rigorous audit approach. As a result, this article's findings are important for standard setters and regulators interested in driving higher levels of audit quality. Rather than focusing exclusively on the technical detail of different standards, the impact that legal liability and auditor's own need to manage impressions may have on how engagements are executed must be carefully considered.

Like any study of this type, there are inherent limitations and areas for future research. Most notably, the operationalisation of only two standards is dealt with. The findings are generated from a single jurisdiction and a relatively small group of respondents. Other standards, such as those dealing with risk assessment, the audit of estimates and documentation need to be examined. More nuanced findings can also be generated by considering how differences in an auditor's age, level of experience and cultural background affects their views on legal exposure and the need to seek legitimacy for their audit work. This can be complemented by considering how recent external regulatory measures interact with individuals' interpretation of professional standards.

Prior research has largely neglected the practical dimension of an external audit with the result that this is an area where academics can make a significant contribution to both theory and practice.

Acknowledgements

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this research article.

Authors' contributions

M.K. conceived the idea for the study. Data were collected by M.K. and W.M., who also wrote the manuscript.

Ethical consideration

This article followed all ethical standards for carrying out research.

Funding information

This research received funding from the National Research Foundation: Grant #118525.

Data availability

The data in this article derives from interviews and are not made available due to ethical restrictions.

Disclaimer

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any affiliated agency of the authors. The views and opinions expressed by respondents quoted in this article are not necessarily those of the authors.

References

Becker, C.L., DeFond, M.L., Jiambalvo, J. & Subramanyam, K., 1998, 'The effect of audit quality on earnings management', Contemporary Accounting Research 15(1), 1-24. https://doi.org/10.1111/j.1911-3846.1998.tb00547.x [ Links ]

Bedard, J.C., Deis, D.R., Curtis, M.B. & Jenkins, J.G., 2008, 'Risk monitoring and control in audit firms: A research synthesis', Auditing: A Journal of Practice & Theory 27(1), 187-218. https://doi.org/10.2308/aud.2008.27.1.187 [ Links ]

Bentley, K.A., Omer, T.C. & Sharp, N.Y., 2013, 'Business strategy, financial reporting irregularities, and audit effort', Contemporary Accounting Research 30(2), 780-817. https://doi.org/10.1111/j.1911-3846.2012.01174.x [ Links ]

Botez, D., 2008, 'Challenges of international standards on auditing in global crisis context', Studies and Scientific Researches. Economics Edition 2008(13), 11-16. https://doi.org/10.29358/sceco.v0i13.9 [ Links ]

Brennan, N.M. & Solomon, J., 2008, 'Corporate governance, accountability and mechanisms of accountability: An overview', Accounting, Auditing & Accountability Journal 21(7), 885-906. [ Links ]

Burns, J. & Fogarty, J., 2010, 'Approaches to auditing standards and their possible impact on auditor behavior', International Journal of Disclosure and Governance 7(4), 310-319. https://doi.org/10.1057/jdg.2010.21 [ Links ]

Byington, J.R. & Sutton, S.G., 1991, 'The self-regulating profession: An analysis of the political monopoly tendencies of the audit profession', Critical Perspectives on Accounting 2(4), 315-330. https://doi.org/10.1016/1045-2354(91)90006-Y [ Links ]

Carson, E., Fargher, N.L., Geiger, M.A., Lennox, C.S., Raghunandan, K. & Willekens, M., 2012, 'Audit reporting for going-concern uncertainty: A research synthesis', Auditing: A Journal of Practice & Theory 32(Sp1), 353-384. https://doi.org/10.2308/ajpt-50324 [ Links ]

Christensen, B.E., Glover, S.M., Omer, T.C. & Shelley, M.K., 2016, 'Understanding audit quality: Insights from audit professionals and investors', Contemporary Accounting Research 33(4), 1648-1684. https://doi.org/10.1111/1911-3846.12212 [ Links ]

DeAngelo, L.E., 1981, 'Auditor size and audit quality', Journal of Accounting and Economics 3(3), 183-199. https://doi.org/10.1016/0165-4101(81)90002-1 [ Links ]

DeFond, M. & Zhang, J., 2014, 'A review of archival auditing research', Journal of Accounting and Economics 58(2-3), 275-326. https://doi.org/10.1016/j.jacceco.2014.09.002 [ Links ]

Geiger, M.A. & Raghunandan, K., 2002, 'Auditor tenure and audit reporting failures', Auditing: A Journal of Practice & Theory 21(1), 67-78. https://doi.org/10.2308/aud.2002.21.1.67 [ Links ]

Geiger, M.A. & Rama, D.V., 2006, 'Audit firm size and going-concern reporting accuracy', Accounting Horizons 20(1), 1-17. https://doi.org/10.2308/acch.2006.20.1.1 [ Links ]

Hogan, C.E. & Wilkins, M.S., 2008, 'Evidence on the audit risk model: Do auditors increase audit fees in the presence of internal control deficiencies?', Contemporary Accounting Research 25(1), 219-242. https://doi.org/10.1506/car.25.1.9 [ Links ]

Holland, J. & Campbell, J., 2005, Methods in development research: Combining qualitative and quantitative approaches, Practical Action, Rugby. [ Links ]

Humphrey, C., Kausar, A., Loft, A. & Woods, M., 2011, 'Regulating audit beyond the crisis: A critical discussion of the EU green paper', European Accounting Review 20(3), 431-457. https://doi.org/10.1080/09638180.2011.597201 [ Links ]

Humphrey, C., Loft, A. & Woods, M., 2009, 'The global audit profession and the international financial architecture: Understanding regulatory relationships at a time of financial crisis', Accounting, Organizations and Society 34(6-7), 810-825. https://doi.org/10.1016/j.aos.2009.06.003 [ Links ]

Humphrey, C. & Moizer, P., 1990, 'From techniques to ideologies: An alternative perspective on the audit function', Critical Perspectives on Accounting 1(3), 217-238. https://doi.org/10.1016/1045-2354(90)03021-7 [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009a, International framework for assurance engagements, 2009 Edition, Volume 2A. SAICA members' handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009b, ISA 200: Overall objectives of the independent auditor and the conduct of an audit in accordance with International Standards on Auditing. SAICA members' handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009c, ISA 220: Quality control for audits of historical financial information. SAICA members' handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009d, ISA 230: Audit documentation. SAICA members' handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009e, ISA 300: Planning an audit of financial statements. SAICA Members' Handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009f, ISA 330: The auditor's responses to assessed risks. SAICA members' handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009g, ISA 500: Audit evidence. SAICA members' handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009h, ISA 510: Initial audit engagements - Opening balances. SAICA members' handbook, 2009 edn., Lexis Nexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009i, ISA 620: Using the work of an auditor's expert. SAICA members' handbook, 2009 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2009j, ISQC1: Quality control for firms that perform audits and reviews of historical financial information, and other assurance and related services engagements. SAICA members' handbook, LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2013, ISA 315R: Identifying and assessing the risk of material misstatement through understanding the entity and its environment. SAICA members' handbook, LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2014, Framework for audit quality: Key elements that create an environment for audit quality, viewed 15 August 2015, from https://www.ifac.org/system/files/publications/files/A-Framework-for-Audit-Quality-Key-Elements-that-Create-an-Environment-for-Audit-Quality-2.pdf [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2015, Exploring assurance on integrated reporting and other emerging developments in external reporting, viewed 11 November 2017, from https://www.iaasb.org/system/files/publications/files/IAASB-Integrated-Reporting-Working-Group-Publication_0.pdf [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2018, ISA 540R: Auditing accounting estimates and related disclosures SAICA Members' Handbook, 2019 edn., LexisNexis, Pietermaritzburg. [ Links ]

International Auditing and Assurance Standards Board (IAASB), 2019, ISA 315R: Identifying and assessing the risks of material misstatement, viewed 30 June 2020, from https://www.ifac.org/system/files/publications/files/ISA-315-Full-Standard-and-Conforming-Amendments-2019-.pdf [ Links ]

International Federation of Accountants (IFAC), 2008, Basis for conclusions: ISA 510 (redrafted), initial audit engagements - Opening balances, International Federation of Accountants, New York, NY. [ Links ]

Jackson, A.B., Moldrich, M. & Roebuck, P., 2008, 'Mandatory audit firm rotation and audit quality', Managerial Auditing Journal 23(5), 420-437. https://doi.org/10.1108/02686900810875271 [ Links ]

Jones, J., Massey, D.W. & Thorne, L., 2003, 'Auditors' ethical reasoning: Insights from past research and implications for the future', Journal of Accounting Literature 22, 45-103. [ Links ]

Kleinman, G., Lin, B.B. & Palmon, D., 2014, 'Audit quality: A cross-national comparison of audit regulatory regimes', Journal of Accounting, Auditing & Finance 29(1), 61-87. https://doi.org/10.1177/0148558X13516127 [ Links ]

Knechel, W.R., Krishnan, G.V., Pevzner, M., Shefchik, L.B. & Velury, U.K., 2012, 'Audit quality: Insights from the academic literature', Auditing: A Journal of Practice & Theory 32(Sp1), 385-421. https://doi.org/10.2308/ajpt-50350 [ Links ]

Lawrence, A., Minutti-Meza, M. & Zhang, P., 2011, 'Can big 4 versus non-big 4 differences in audit-quality proxies be attributed to client characteristics?', The Accounting Review 86(1), 259-286. https://doi.org/10.2308/accr.00000009 [ Links ]

Leedy, P.D. & Ormrod, J.E., 2015, Practical research, planning and design, Pearson Education, Essex. [ Links ]

Maroun, W., 2012, 'Interpretive and critical research: Methodological blasphemy!', African Journal of Business Management 6(1), 1. https://doi.org/10.5897/AJBM11.1031 [ Links ]

Maroun, W. & Jonker, C., 2014, 'Critical and interpretive accounting, auditing and governance research in South Africa', Southern African Journal of Accountability and Auditing Research 16(1), 51-62. [ Links ]

Maroun, W. & Solomon, J., 2014, 'Whistle-blowing by external auditors: Seeking legitimacy for the South African audit profession?', Accounting Forum 38(2), 109-121. [ Links ]

Martinov-Bennie, N. & Pflugrath, G., 2009, 'The strength of an accounting firm's ethical environment and the quality of auditors' judgments', Journal of Business Ethics 87(2), 237-253. https://doi.org/10.1007/s10551-008-9882-1 [ Links ]

Mock, T.J., Bédard, J., Coram, P.J., Davis, S.M., Espahbodi, R. & Warne, R.C., 2012, 'The audit reporting model: Current research synthesis and implications', Auditing: A Journal of Practice & Theory 32(Sp1), 323-351. https://doi.org/10.2308/ajpt-50294 [ Links ]

Nelson, M.W., 2009, 'A model and literature review of professional skepticism in auditing', Auditing: A Journal of Practice & Theory 28(2), 1-34. https://doi.org/10.2308/aud.2009.28.2.1 [ Links ]

O'Dwyer, B., Owen, D. & Unerman, J., 2011, 'Seeking legitimacy for new assurance forms: The case of assurance on sustainability reporting', Accounting, Organizations and Society 36(1), 31-52. https://doi.org/10.1016/j.aos.2011.01.002 [ Links ]

Palmrose, Z.-V., 1988, 'An analysis of auditor litigation and audit service quality', The Accounting Review 63(1), 55. [ Links ]

Palmrose, Z.-V., 1997, 'Audit litigation research: Do the merits matter? An assessment and directions for future research', Journal of Accounting and Public Policy 16(4), 355-378. https://doi.org/10.1016/S0278-4254(97)00037-9 [ Links ]

Peecher, M.E., Schwartz, R. & Solomon, I., 2007, 'It's all about audit quality: Perspectives on strategic-systems auditing', Accounting, Organizations and Society 32(4), 463-485. https://doi.org/10.1016/j.aos.2006.09.001 [ Links ]

Piot, C. & Janin, R., 2007, 'External auditors, audit committees and earnings management in France', European Accounting Review 16(2), 429-454. https://doi.org/10.1080/09638180701391030 [ Links ]

Power, M., 1991, 'Auditing and environmental expertise: Between protest and professionalisation', Accounting, Auditing & Accountability Journal 4(3), 30-42. https://doi.org/10.1108/09513579110141751 [ Links ]

Power, M., 1994, The audit explosion, Demos, London. [ Links ]

Power, M., 1995, 'Auditing, expertise and the sociology of technique', Critical Perspectives on Accounting 6(4), 317-339. https://doi.org/10.1006/cpac.1995.1029 [ Links ]

Power, M., 2003a, 'Evaluating the audit explosion', Law & Policy 25(3), 185-202. https://doi.org/10.1111/j.1467-9930.2003.00147.x [ Links ]

Power, M.K., 2003b, 'Auditing and the production of legitimacy', Accounting, Organizations and Society 28(4), 379-394. https://doi.org/10.1016/S0361-3682(01)00047-2 [ Links ]

Rowley, J., 2012, 'Conducting research interviews', Management Research Review 35(3/4), 260-271. https://doi.org/10.1108/01409171211210154 [ Links ]

Ryan, B., Scapens, R.W. & Theobald, M., 2002, Research method and methodology in finance and accounting, Cengage, Andover. [ Links ]

Simnett, R., Carson, E. & Vanstraelen, A., 2016, 'International archival auditing and assurance research: Trends, methodological issues, and opportunities', Auditing: A Journal of Practice & Theory 35(3), 1-32. https://doi.org/10.2308/ajpt-51377 [ Links ]

Thomas, D.R., 2006, 'A general inductive approach for analyzing qualitative evaluation data', American Journal of Evaluation 27(2), 237-246. https://doi.org/10.1177/1098214005283748 [ Links ]

Turner, J.L., Mock, T.J., Coram, P.J. & Gray, G.L., 2010, 'Improving transparency and relevance of auditor communications with financial statement users', Current Issues in Auditing 4(1), A1-A8. https://doi.org/10.2308/ciia.2010.4.1.A1 [ Links ]

Unerman, J. & O'Dwyer, B., 2004, 'Enron, WorldCom, Andersen et al.: A challenge to modernity', Critical Perspectives on Accounting 15(6), 971-993. https://doi.org/10.1016/j.cpa.2003.04.002 [ Links ]

Watts, R.L. & Zimmerman, J.L., 1983, 'Agency problems, auditing, and the theory of the firm: Some evidence', Journal of Law and Economics 26(3), 613-633. https://doi.org/10.1086/467051 [ Links ]

Correspondence:

Correspondence:

Warren Maroun

warren.maroun@wits.ac.za

Received: 28 July 2020

Accepted: 30 Nov. 2020

Published: 18 Mar. 2021

1 . The choice of method was also informed by the fact that working papers providing detail on the application of auditing standards are not publicly available for quantitative analysis.

2 . The Big 4 include, in alphabetical order, Deloitte, EY, KPMG and PwC. The researchers distinguished between second-tier and small firms based on revenue.

{kind=link}