Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

On-line version ISSN 2411-9717

Print version ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.114 n.11 Johannesburg Nov. 2014

MINING ENVIRONMENT AND SOCIETY CONFERENCE 2013

Tiger's eye in the Northern Cape Province - potential for employment creation and poverty alleviation

P.F. Ledwaba

Small-Scale Mining and Beneficiation Division, Mintek

SYNOPSIS

South Africa's Northern Cape Province houses a variety of gemstone minerals. Diamonds remain the primary gemstone in the province, but there are also tiger's eye, sugilite, rose quartz, jasper, amethyst, amazonite, tourmaline, and topaz deposits. This paper gives an overview of the tiger's eye (TE) mining sector in the Northern Cape, with the objective of assessing the potential of TE to contribute to job creation and poverty alleviation in the province. Mining of TE started in 1803, but gained momentum during the 1960s. Mining is conducted on a small-scale basis, and in most cases without any legal framework. The majority of the residents are not benefiting from TE. It has been reported that an estimated R700 000 to R800 000 worth of TE is leaving the country every week through illegal trading. The potential for TE mining to contribute to socioeconomic development is hindered by illegal operations, lack of technical skills and knowledge, exploitation by dealers, lack of market information, community rivalries, and absence of value addition. A multi-stakeholder approach is needed to formalize the sector and reap the benefits. Mintek is spearheading a TE project in the Prieska area of the Northern Cape, which aims to establish a gemmological centre where TE can be beneficiated into saleable and high-value products.

Keywords: Northern Cape, small-scale mining, tiger's eye, socio-economic development, multi-stakeholder approach

Introduction

South Africa is well endowed with mineral resources. The country's mineral endowment includes precious metals and minerals, energy minerals, non-ferrous metals and minerals, ferrous minerals, industrial minerals, and semi-precious minerals, with a total estimated worth of 2.5 trillion US dollars (Department of Mineral Resources, 2011). Semi-precious minerals have been neglected because of their low economic value compared to the traditional gold and diamonds. Semi-precious minerals are also referred to as gemstones. The UN Standard International Classification System defines gemstones as 'all precious and semiprecious stones (whether or not they have been worked or graded) excluding: all categories of diamonds, all precious stones composed of non-minerals and all precious stones made of synthetic or reconstructed material' (Cross, Van der Wal, and De Haan, 2010). Examples of gemstones include (but are not limited to) tiger's eye, sugilite, rose quartz, jasper, amethyst, amazonite, tourmaline, and topaz. This paper focuses specifically on tiger's eye (TE).

The Northern Cape Province houses significant TE resources, which are among the few in the world with economic potential. TE mining in the province started as early as 1803 (Loo, 1998), and has been conducted since then on a small-scale basis. The small-scale mining (SSM) sector in South Africa has been identified as having potential to address triple developmental challenges, namely job creation, poverty alleviation, and inequality reduction. The sector provides a platform for the historically disadvantaged South Africans (HDSAs) to participate in and benefit from the minerals and mining industry. The objective of this paper is to assess the potential of TE to contribute to job creation and poverty alleviation in the province. This is done by assessing the mine value chain of TE and hence identifying challenges and opportunities present in the sector.

Study area

TE deposits occur in the banded iron formations in the Northern Cape Province. Significant deposits are located in the Niekerkshoop, Prieska, Griekwastad, and Hay areas of the province (Northern Cape Province Mineral Sector Strategy, 2004), and there are extensive mining activities in the Prieska and Niekerkshoop areas. Most miners are dependent on mining for their livelihoods.

Overview of the TE sector

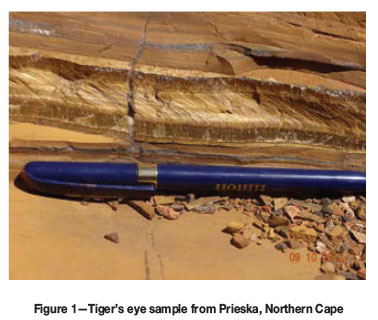

TE is a form of asbestos that has been silicified by iron-bearing quartz, leaving the fibrous appearance intact. The attractive cat's eye effect, called the chatoyant effect or chatoyancy, is caused by the reflection of lightfrom the fibres. TE comes in a variety of colours, which depend on slight differences in the oxidation state of the iron (Rocksandminerals4u, n.d.). The common colours include gold, yellow, and brown; red and blue/grey are rarer. Figure 1 shows a TE sample from Prieska.

Mining of TE

TE is mined on a small scale using rudimentary tools to extract and dress the stone. The process involves the removal of the overburden to expose the TE, which is hosted in the banded ironstone, also referred to as 'dead stones' by the miners. In areas where the host rocks are too hard to remove, miners burn wood and old tyres on top of the rock mass to crack the rocks. This allows the TE to be extracted using chisels and hammers. Some miners make use of hydraulic jacks to separate the rocks. Mining is done haphazardly using trial-and-error methods. The miners use colour to prospect and identify mining sites. Once the TE is removed, it is sent for dressing. This is usually conducted by women as it is less labour-intensive than the mining. Dressing involves the removal of the 'dead stone' from the TE.

TE mining in the Northern Cape occurs on both communal land and private farms. Communal land in the Prieska and Niekerkshoop districts covers an area of approximately 32 000 hectares, with private farms occupying about 5 000 hectares (Basson, 2013). Mining on communal land is not regulated, and most miners continue to operate without any legal framework. The Department of Mineral Resources (DMR) has records of 15 mining permits, all of which are located on private farms (Mahala, 2012). There appear to be over 100 miners exploiting TE on communal land. It is difficult to quantify the number of unlicensed operations, because most miners work as individuals, although some have formed groups. Moreover, the numbers fluctuate from time to time because anyone seems to be able to enter the area and mine.

Value addition

South Africa had a local TE processing industry prior to 1996. In 1971, the government introduced the Tiger's Eye Control Act, which banned the export of unprocessed TE. The objective of the export restriction was to develop the stone cutting and polishing industry and hence increase the country's benefits from TE. Unfortunately, the provision was not able to deliver on the set objectives. According to Loo (1998), it gave rise to illegal mining and illegal trading. This led to the closure of the TE processing facilities. Local manufacturers decreased from 15 in 1990 to 5 in 1995. At present all known manufacturers have closed down (Loo, 1998). The export of raw TE is still banned. However, due to the lack of government capacity to enforce the ban, raw TE continues to be exported.

TE grades and pricing

The miners produce six grades of TE: grade A, grade B, grade C, grade X, variegated, and blue. The thickness of the seam (or 'reef') and chatoyancy are used to grade the stones (Cornelissen, 2013). The different grades are shown in Table I. The prices are those paid to the miners by the dealers.

Grade A is high-quality stone. Stones with thickness of 15 mm or greater are graded A. The price for grade A material ranges from R10.00 to R18.00 per kilogram. The price is usually dictated by the buyers and because TE mining is poverty-driven, it constitutes a 'buyer's market'. Grade X is the lowest quality. It contains inclusions which are often regarded as 'dead stones', and sells for between R0.50 and R 1.00 per kilogram.

Table II summarizes selling prices for variegated and blue TE. Variegate is TE with two colours, usually a mixture of yellow and blue. It sells for R2.50 to R3.00 per kilogram.

There is no conclusive information on TE export prices. A study conducted by the Northern Cape Provincial Government (2004) reported TE export prices in the range US$0.50 to US$12 per kilogram, depending on the quality of the stone.

Supply and demand

There are currently no production figures available for TE. Production figures were last recorded in 1996 by the Minerals Bureau. Daily production is dependent on the areas being mined and the number of miners working together. It is difficult to estimate production rates because some miners work in groups and some as individuals. However, most of the miners sell their stone to one buyer/dealer. It is reported that at least two to three containers leave Prieska every week. A container can take approximately 420 bags, each weighing 50 kg. This equates to 21 t per container. If three containers leave the area weekly, then monthly production will amount to 252 t. (Please note that this calculation is not conclusive: it was informed by the data obtained from the miners during field work.)

The containers are transported to Cape Town for export. There is very limited information on the TE export market. However, literature reports that main markets are the USA, Japan, and China, with China constituting the largest share of the market. The local market is small, almost non-existent.

TE is widely used in ornamental jewellery. It is also used to make pendants, beads for jewellery, and other small items.

Market structure

Figure 2 illustrates the market structure of the TE industry in Prieska.

The miners sell their stones to the primary dealers. A dealer is defined as a person or a firm that is involved in the buying and selling. There are two dealers operating in the Prieska; that is the primary and secondary dealers. The primary dealer buys directly from the miners, and the secondary dealer is the gateway to the export market. Secondary dealers have knowledge of the export market.

Legislation governing the TE industry

Tiger's eye mining in South Africa started as early as 1803. During the 1960s, mining activities increased considerably. This led to the introduction of the Tiger's Eye Control Act of 1977, which banned the export of unprocessed TE. This was done to develop the local cutting industry and hence increase jobs and government revenue. However, because of inadequate capacity (infrastructure, skills, high cost of consumables, access to markets etc.), many processing factories closed. This resulted in the smuggling and illegal selling of TE. To date, the government has not been able to control illegal trading of unprocessed TE.

In 1994, after the major political change in South frica, the new government rationalized minerals and energy legislation. Past laws were reviewed and Tiger's Eye Control Act was repealed and replaced by the Minerals Act (Act 50 of 1991). This in turn was later replaced by the Mineral and Petroleum Resources Development Act (MPRDA) in 2004, which currently governs all mining activities, including TE. There are no special provisions for TE mining and benefi-ciation in the MPRDA. However, the MPRDA supports the development of a mineral beneficiation industry in the country (Government Gazette, 2002). Mineral-rich countries are prioritizing value addition and are looking at different mechanisms to develop mineral beneficiation industries. South Africa has placed export restrictions on several minerals, including TE, under the International Trade Administration Act No. 71 of 2002 (Government Gazette, 2003). According to the Act; 'Tiger's eye shall not be exported from the Republic of South Africa, except by virtue of an export permit issued in terms of Section 6 of the Act'. TE is defined in the Act as follows: 'Tiger's eye including its related varieties and also any articles consisting wholly or partly of tiger's eye or its related varieties but excluding properly finished andfinally and completely polished cabochons, beads, eggs, spheres, tumbled stone and carvings cut therefrom or otherwise processed or tumbled (Government Gazette, 2012).

Other legislations governing mining activities include the National Environmental Management Act, National Water Act, Mine Health and Safety Act, National Heritage Resource Act, Waste Act, Biodiversity Act, and Air Quality Act. At present, none of the applicable legislations are followed and adhered to in the TE sector.

Potential of TE sector

The TE resources of the Northern Cape Province are among the few in the world with economic value. There are currently no resource estimations, although it is reported that there still exist large deposit of TE. An estimated 37 000 hectares of land in Prieska and Niekerkshoop holds significant TE deposits. The depth of TE mining is limited by the mining methods, which involve the use of primary tools to remove TE from the ground. Hence there may still significant TE resources at greater depths.

Mining of TE is relatively a simple process, and does not require expensive equipment. At present, the industry employs over 100 miners. A substantial number of these are women and youths. However, because the miners are being exploited, mining has little visible impact in their lives. They are mining for day-to-day survival. The main hurdle in the sector is the lack of supervision and action by government to enforce legislation. The DMR is currently assisting miners in Prieska to obtain a mining license. This is a positive step towards addressing the ills in the sector.

Mineral beneficiation has been identified as one of the drivers for job creation. Jewellery fabrication has been earmarked as one of the strategic value chains in South Africa's beneficiation strategy, which proposes the establishment of integrated jewellery hubs across the country (Department of Mineral Resources (2011). The current focus is on gold and platinum. However, there are notable interventions directed to other minerals used in jewellery manufacture, such as semi-precious minerals. The establishment of a TE beneficiation centre will generate additional jobs.

Profitability

TE miners are not making significant amounts of money. The returns from mining range from R500 to R1500 per week, depending mainly on production rates and the quality of the stone. Typical weekly production varies from 50 kg to 100 kg. This applies to miners who work in groups (usually a group of four or five). Miners who work as individuals produce less and hence make very little money. However, it has been reported that significant amounts of TE leave the country every week. The local market is controlled by a few individuals who have export connections. The value of the industry is currently unknown. However, an estimated R700 000 to R 800 000 worth of TE is reported to leave the country every week through smuggling (Spicer, 2003). If that is the case, then the total value of TE leaving South Africa per month is over R3 million. These figures indicate that there is a substantial market for TE, which South Africa is not benefiting from.

Marketability

The issue of marketability is linked to long-term sustain-ability. Marketability remains a gap in the sector. Current demand is dominated by the international market. Local interest is not established. TE should be marketed both locally and internationally to build a solid market. TE is rarer than most semi-precious stones, and is among the gemstones that are regarded as attractive, owing to its unique chatoyancy and lustre. Marketability is affected by the issues of illegal mining and smuggling. The miners allege that the TE that is exported from the country is stockpiled overseas, although this has neither been proved nor disproved. However, if this is the case, it will impact on the TE marketability, and could place the country's comparative advantage at a risk.

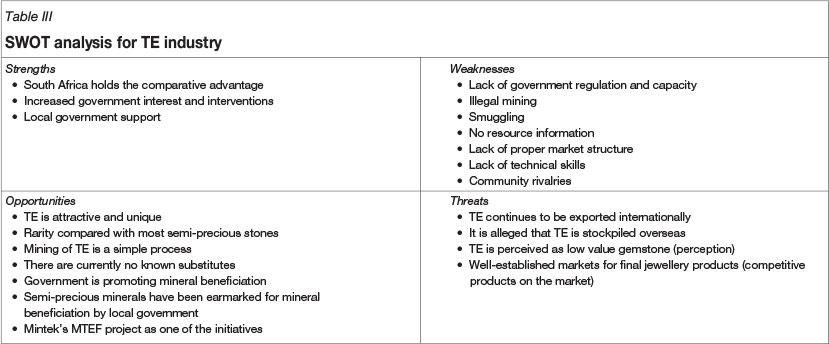

SWOT analysis

Table III summarizes the strengths, weaknesses, opportunities, and threats of the TE sector.

There are a number of issues in the TE sector. However, the key issues that need the most attention are: (1) government capacity (2) resource information, (3) market information, (4) beneficiation, and (5) community rivalries. In relation to the key issues, it is proposed that the following activities be undertaken:

Increase government participation and involvement Invest in research and development (R&D) Marketing should take the lead in R&D Increase collaboration between government structures and other relevant stakeholders.

Mintek TE project

The Northern Cape Province has been identified as a priority area for socio-economic development by the South African Treasury under the Medium Term Expenditure Framework (MTEF). The province is home to significant semi-precious mineral deposits, most of which are exploited on a small-scale level and informally in most areas, resulting in very little socio-economic benefit.

The objective of Mintek's TE project is to establish a gemmological centre where semi-precious minerals can be beneficiated into saleable and high-value end-products. Mintek is spearheading the project, which is funded by the MTEF. This is a three-year project and is divided into two phases. The first phase consisted essentially of research and development to identify and locate all potential deposits of semi-precious minerals. The second phase is the implementation phase, in which beneficiation centres will be established in the province. The first phase has been completed and TE in the Prieska region has been selected as a priority area because it holds potential socio-economic benefits. Mintek is working with the Department of Mineral Resources and communities and stakeholders from the Siyathemba Local Municipality to set up the beneficiation centre in Prieska. The potential benefits from the project are: (1) job creation, (2) skills development and transfer, (3) development of small, micro, and medium enterprises (SMMEs), and (4) promotion of local beneficiation.

Conclusion

Since mining commenced during 1803, socio-economic benefits from tiger's eye have not been realized. The majority of the people in the Northern Cape are not benefiting. To date, mining of TE has constituted a means to livelihoods. The biggest hurdle in the sector is the lack of effective government regulation. Although legislation exists, government lacks the capacity to enforce and monitor legislation. It is important for government to recognize the potential of TE. This is a socio-economic imperative, not only for the Northern Cape Province, but for the national mainstream economy. The contribution of the TE industry to socio-economic development is hindered by illegal operations, lack of technical skills and knowledge, exploitation by dealers, lack of market information, community rivalries, and the absence of a beneficiation industry. Because of the nature of these challenges, a multi-stakeholder approach is needed. However, it should be the responsibility of government to spearhead the initiative. Government should identify and facilitate all relevant stakeholders.

Acknowledgements

This research was supported by Mintek's MTEF Project under the Small-Scale Mining and Beneficiation Division (SSMB). I would like to express my gratitude to the following stakeholders:

Mr Ncedisa Mahala, Department of Mineral Resources

Dr Hudson Mtegha, University of Witwatersrand

Professor Jason Ogola, University of Venda

Mr Jakob Basson, Siyathemba Local Municipality

Mr Abram Booysen, tiger's eye miner

Mr Jiyane Tshenge, Prieska community leader

Mr Patrick Pieterse, Niekerkshoop Ubuntu Tiger's Eye

Mining

References

Basson, J. 2013. Local Economic Development Officer, Siyathemba Local Municipality, Prieska, Northern Cape. Personal communication, 22 August 2013. [ Links ]

Cornelissen, H. 2013. Report on site visits conducted on tiger's eye mining operations in the Northern Cape Province to assess the risk associated with mining of the tiger's eye deposit. Internal report, Mintek, Randburg, 10 March 2013. [ Links ]

Cross, J., Van der Wal, S., and De Haan, E. 2010. Sustainability Issues in the Coloured Gemstone Industry. Centre for Research on Multinational Corporations (SOMO), Amsterdam, February 2010. [ Links ]

Department of Mineral Resources. 2011. A Beneficiation Strategy for the Minerals Industry of South Africa. Pretoria, June 2011. [ Links ]

Government Gazette. 2002. Mineral and Petroleum Resources Development Act No. 28 of 2002 (MPRDA), Republic of South Afnca.No. 448, 10 October 2002. [ Links ]

Government Gazette. 2003. International Trade Administration Act No. 17 of 2002, Republic of South Africa. No. 24287, 22 January 2003. [ Links ]

Government Gazette. 2012. Export control, International Trade Administration Commission of South Africa. No. 35007, 10 February 2012. [ Links ]

Loo, J.P. 1998. To revitalise the tiger's eye industry: A preliminary update and review of previous documentation. Mineral Processing Division, Mintek, Randburg, 30 April 1998. [ Links ]

Mahala, N. 2012. Department of Mineral Resources, Small Scale Mining Directorate, Northern Cape Regional Office, Kimberley. Personal communication, 9 October 2012. [ Links ]

Northern Cape ProvincialGovernment. 2004., Mining and Minerals Sector Strategy for the Northern Cape Province, October 2004. 77 pp. [ Links ]

Rocksandminerals4u. Not dated. Tiger's Eye. http://www.rocksandminerals4u.com/tigers_eye.html [Accessed 10 August 2013]. [ Links ]

Spicer, D. 2003. Fears expressed that SA is losing out in illegal tiger's eye trade. Mining Weekly Online, 28 March 2003. [ Links ]

© The Southern African Institute of Mining and Metallurgy, 2014. ISSN2225-6253. This paper was first presented at the, Mining, Environment and Society Conference 2013, 27-28 November 2013, Misty Hills Country Hotel and Conference Centre, Cradle of Humankind, Muldersdrift.

{kind=link}